Global equity markets continued to come under pressure in October, weighed down by increasing Covid-19 infections in Europe and the US, with many countries across Europe reintroducing lockdown measures.

Markets also reacted negatively to concerns around the lack of further announced fiscal stimulus, as well as the outcome of the US Presidential Election in early November and its effect on economic policy.

The much talked about US large-cap technology names, which have led the global equity market recovery since March, also came under pressure during the month. Apple, Amazon and Facebook struggled, weighed down by earnings releases that the market perceived as disappointing.

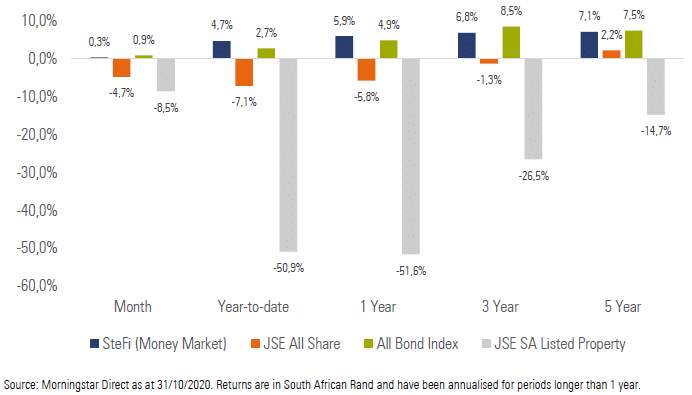

Exhibit 1: SA Market Performance (total returns)

South African equities moved lower during the month, in line with the risk off mood in global markets. The performance of local equities was weighed down by poor performance from large cap resource counters on the back of softer commodity prices.

Local bonds fared relatively well despite the volatility in global markets, ending the month as the best performing local asset class. Short and medium dated instruments benefitted from the increased possibility of an interest cut rate, given well contained inflation.

Local listed property continues to be a laggard, weighed down by elevated debt ratios, asset write downs and the possibility of a dilution through capital raises at depressed share price levels.

The rand fared well against most major developed market currencies for the month, which acted as a headwind for the performance of global asset classes in rand terms.

Finance Minister Tito Mboweni delivered the Medium-Term Budget Policy Statement towards the end of October. The speech contained detail on planned expenditure cuts, which are largely driven by reductions in the public sector wage bill and efforts to divert spending away from consumption to infrastructure.

Minister Mboweni also announced further financial support for SOE’s, with SAA receiving R10.5 billion rand to assist the airline’s business rescue process and an additional R7 billion allocated to Land Bank.

In terms of economic growth, available data appears to indicate that economic activity rebounded strongly in the 3rd quarter, which suggests that Q3 GDP growth may significantly outperform consensus forecasts. Despite the significant recovery in the third quarter, the lockdown in Q2 is likely to lead to the sharpest economic contraction in the 2020 calendar year for quite some time.

SA headline CPI fell to a year-on-year figure of 3.0% to the end of September (from 3.1% in August), largely driven by slower than expected rental inflation.

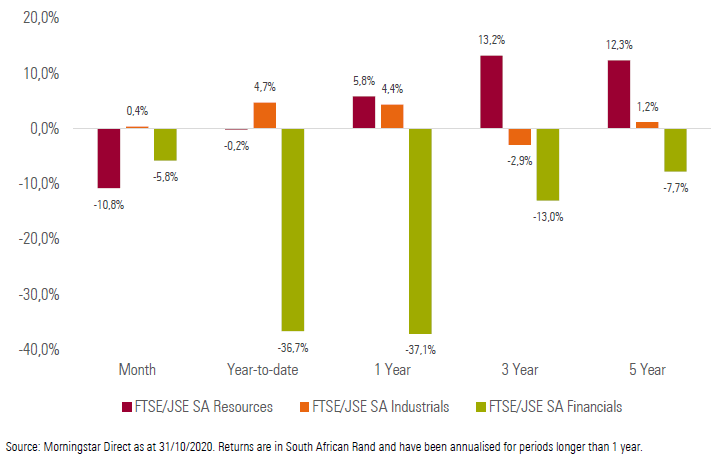

Local equity sectors had mixed performance during the month, with Industrials (+0.4%) ending the month higher, while Financials (-5.8%) and Resources (-10.8%) ended the month sharply lower.

Exhibit 2: SA Sector Performance (total returns)

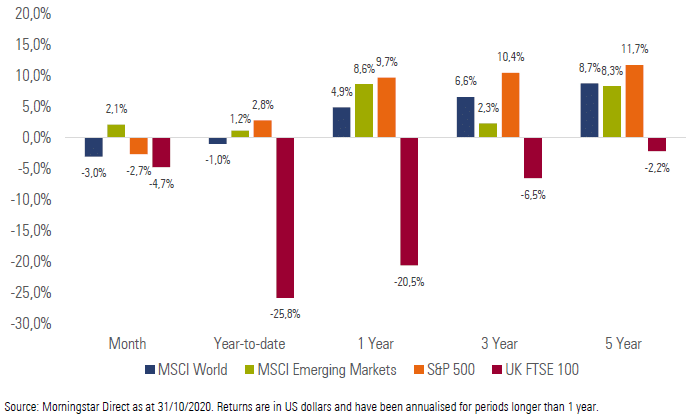

Most major developed equity markets ended the month lower, amid concerns around the economic impact of spiking Covid-19 infections and the reintroduction of lockdown measures in some countries. The MSCI World Index delivered a return of -3.0% for the month.

Emerging market equities bucked the global trend, ending the month higher on the back of decent performance from Chinese equities. The MSCI Emerging Markets Index delivered a return of +2.1% for the month.

Most major equity markets ended the month lower, with UK’s FTSE 100 (-4.7%) and Germany’s FSE DAX (-10.0%) feeling the brunt of the pain. China’s Shanghai SE Composite (+1.9%) and Japan’s Nikkei 225 (+0.1%) bucked the global trend slightly, as Asian equity markets fared better than those in Europe and the US.

US equities also ended the month lower, with both the tech heavy NASDAQ 100 (-3.2%) and the S&P 500 (-2.7%) ending in the red. The performance of US equities was weighed down by poor performance from the technology sector.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios struggled to generate positive returns for the month, as both local and global risk assets came under pressure. The rand also acted as a headwind to the performance of global assets in rand terms for the month, as the local currency appreciated against most major currencies over the month. Those investors with an income focus fared slightly better than those with significant allocations to equities, as the local bond market held up well despite the risk off environment.

As we head into the final two months of the year, we are aware of the continued uncertainty regarding Covid-19 infection rates, the outcome of the US Presidential Election, as well as the likelihood of any new fiscal stimulus to support economies. While we understand that this uncertainty may be uncomfortable for investors, we would, as always, encourage investors to focus on their long-term investment goals. Patient, long-term, valuation driven investors are likely to be rewarded with above average returns in the long run, independent of the market environment.

Market summary

Click on the link below to download October’s market summary.