Global equity markets ended the month in positive territory, despite rather modest gains in certain major markets, as global economies continued to show signs of recovery despite new Covid-19 restrictions in certain countries.

There continues to be optimism around the US economic recovery, as strong economic data and the high likelihood of further stimulus measures continues to bode well for risk appetite. This, despite Republicans in the Senate unveiling a $928 billion infrastructure proposal, well below US President Joe Biden’s original $1.7 trillion plan.

Inflation continues to be a talking point for investors, as the US Federal Reserve’s (Fed) preferred inflation measure, core personal consumption expenditure (PCE), advanced 0.7% month on month in April, bringing the year-on-year figure to the end of April to 3.1%. The Fed continues to reiterate its belief that inflation pressures are transitory and that they intend to keep monetary policy conditions accommodative for the foreseeable future.

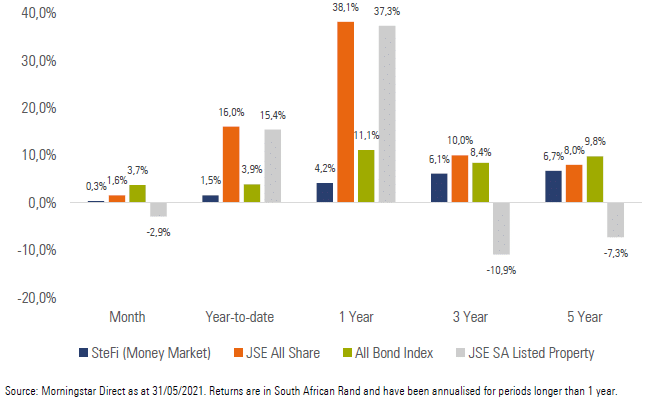

Exhibit 1: SA Market Performance (total returns)

South African equities ended higher for a seventh consecutive month, largely driven by strong performance from Financials, gold counters and retailers.

Local bonds had a strong month, as foreigners returned to the SA market (foreigners bought R9.3 billion of local bonds in May) and the yield curve flattened following strong performance from long dated SA government bonds.

Local listed property gave back some gains during the month, as the asset class took a breather after strong performance in April. Uncertainty caused by the implications of a third wave of Covid- 19 infections acted as a headwind for the asset class.

The rand continued its impressive recent run, finishing the month stronger against most major developed market currencies, supported by strong commodity prices and US dollar weakness.

The South African Reserve Bank’s (SARB) Monetary Policy Committee (MPC) left interest rates unchanged for a fifth consecutive meeting in a unanimous decision, with the MPC revising its growth forecast higher for 2021 from 3.8% to 4.2% following the strong rebound in Q1 2021.

SA headline CPI moved significantly higher to a year-on-year figure of 4.4% for April (from 3.2% in March), the largest monthly change in annual inflation since 2009. The increase was largely driven by the base effects of higher fuel and food prices.

SA’s trade surplus continues to provide support to the rand, with the surplus for April (R51 billion) following a revised surplus for March of R52.5 billion.

Following higher daily Covid-19 cases across the country, President Cyril Ramaphosa announced that South Africa would move to a level two lockdown (effective 31 May), largely in response to a third wave of infections in certain provinces across the country.

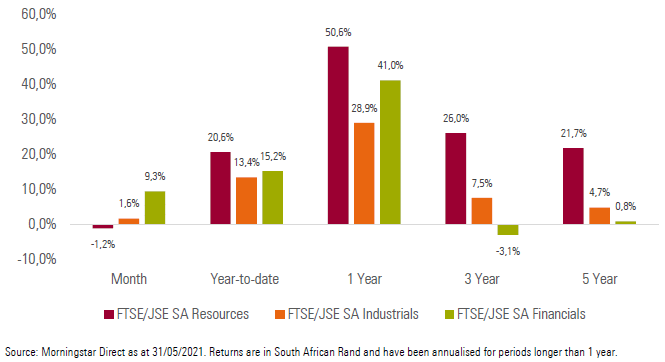

Local equity sectors had mixed performance for the month, with Financials (+9.3%) outperforming both Industrials (+1.6%) and Resources (-1.2%).

Exhibit 2: SA Sector Performance (total returns)

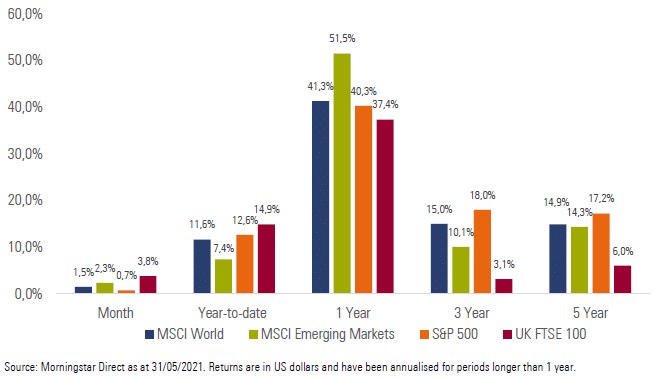

Most major developed equity markets ended the month with positive returns, although the returns were quite divergent across different geographies. The MSCI World Index delivered a return of +1.5% for the month.

Emerging market equities outperformed developed market equities slightly over the month, largely driven by strong returns from Chinese equities. The MSCI Emerging Markets Index delivered a return of +2.3% for the month.

Most major equity markets ended the month higher, with China’s Shanghai SE Composite (+6.7%), the UK’s FTSE 100 (+3.8%) and Germany’s FSE DAX (+3.5%) ending the month with decent returns. Japan’s Nikkei 225 (+0.1%) ended the month largely flat.

US equities had mixed performance for the month. The S&P 500 (+0.7%) ended the month higher, while the NASDAQ 100 (-1.2%) ended the month in the red.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios managed to deliver positive performance for the month. Local equities and bonds contributed positively to performance, while significant rand strength acted as a headwind to the performance of offshore allocations. Income focused investors will be pleased with performance generated during the month, which was largely driven by strong returns from medium and long dated SA government bonds, while local listed property acted as a headwind to performance.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation driven approach by allocating assets to the most attractive areas of the market from a reward for risk perspective. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

Market summary

Click on the link below to download May’s market summary.