Most major global equity markets ended the month with positive returns, as economic data reflecting the recovery from the Covid-19 pandemic continued to surprise on the upside. Equity investors continue to remain bullish, with another US stimulus package on the horizon, despite concerns around a ship stuck in the Suez Canal, which disrupted a major global shipping route for a few days during the month.

March was dominated by market participants taking note of movements in global bond markets, as yields continued to move higher (moving prices lower), led by US Treasuries, as global bonds ended the quarter with their worst return in decades.

The uptick in global bond yields appears to be connected to inflation expectations, with fixed income markets pricing in higher inflation in the medium term, which is likely to lead to interest rate increases from the US Federal Reserve (Fed). This, despite the Fed’s insistence that they will continue to keep monetary policy accommodative as the US economy continues its recovery from the shock of the Covid-19 pandemic.

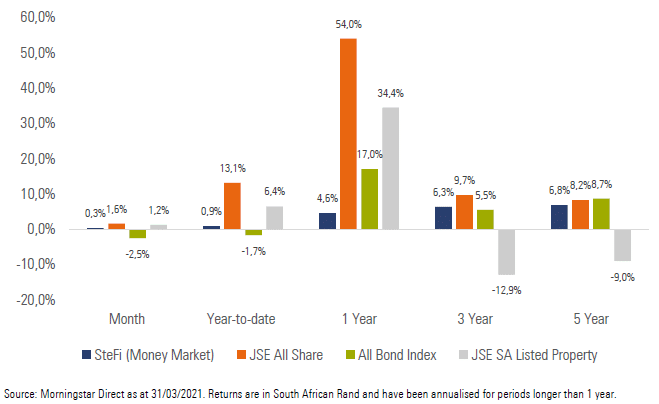

Exhibit 1: SA Market Performance (total returns)

South African equities ended higher for a fifth consecutive month, with positive performance across all three major local equity sectors.

Local bonds ended the month lower, despite positive news on lower-than-expected inflation, a reduction in government bond auctions, a lower-than-expected budget deficit and a stronger rand. The weak performance from bonds was largely driven by SA yields drifting higher (moving prices lower) in reaction to movements in global bond markets.

Local listed property ended the month higher, however, weak performance from some of the larger counters including Growthpoint and Redefine led to muted returns from the SA Listed Property Index.

The rand was stronger against most major developed market currencies, despite weakening significantly against the US dollar at the beginning of March, only to recover the lost ground towards the end of the month.

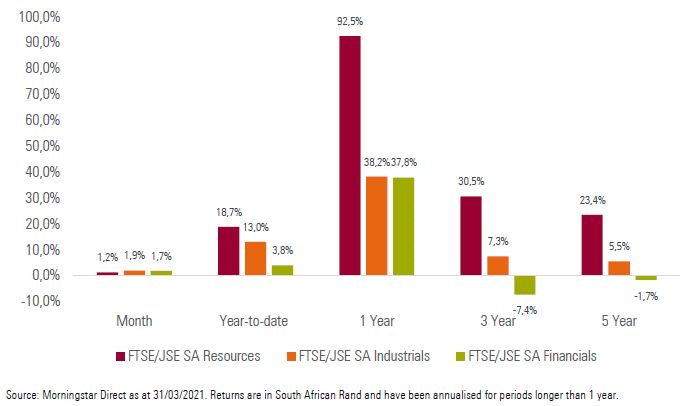

All local equity sectors ended the month higher, with Industrials (+1.9%), Financials (+1.7%) and Resources (+1.2%) finishing the month with positive returns.

Exhibit 2: SA Sector Performance (total returns)

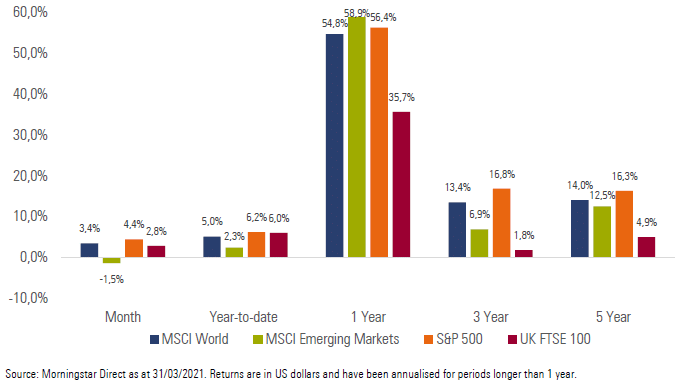

Most major developed equity markets ended the month with positive returns, with US equities being the largest contributor to the performance of the index. The MSCI World Index delivered a return of +3.4% for the month.

Emerging market equities underperformed developed market equities over the month, ending March with a negative return. The MSCI Emerging Markets Index delivered a return of -1.5% for the month.

Major equity markets showed mixed performance for the month, with Germany’s FSE DAX (+5.4%) and the UK’s FTSE 100 (+2.8%) ending the month higher, while Japan’s Nikkei 225 (- 2.3%) and China’s Shanghai SE Composite (-3.3%) ended the month in the red.

US equities delivered decent performance for the month, with both the S&P 500 (+4.4%) and the tech heavy NASDAQ 100 (+1.5%) ending the month in positive territory.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios managed to deliver positive performance for the month. Both local and global equities delivered positive performance in rand terms, which helped to drive the performance of portfolios with significant allocations to risk assets. Income focused investors faced a headwind from rising bond yields (i.e. lower prices), largely due to rising inflation expectations and concerns around interest rates increasing in the medium term. This affected the performance of portfolios with an income focus, with the majority ending the month with either flat or slightly negative performance.

We are pleased with returns generated by portfolios in the first quarter of the year, with performance largely driven by strong returns from both local and global equities. Bonds were a slight laggard over the quarter, with rising inflation and interest rate expectations causing yields to move higher and prices to move lower. We are comfortable with the current positioning of portfolios and have confidence in them delivering on their stated investment objectives over the long term. We will continue to seek to allocate capital using our valuation driven approach, relying on the three pillars of asset allocation, manager selection and portfolio construction to deliver strong absolute and relative returns at lower levels of risk.

Market summary

Click on the link below to download March’s market summary.