Global markets continued to sell off over the month as rising interest rates and persistently higher inflation point to an especially negative outlook for short-term asset prices. Increasing fears of a potential global recession further contributed to elevated volatility across both developed and emerging markets as investors remain sceptical of the ability of central bankers to balance the trade-off between growth and inflation.

The US Federal Reserve hiked interest rates by a further 0.75% at the meeting in early June to follow the 0.50% increase in May. Inflation continues to be less transient than some market pundits were initially suggesting as global supply chain shortages persist and energy and food prices remain elevated due to the ongoing Russian invasion of Ukraine. The US inflation print came in at 8.6% (year-on-year to the end of May), the highest reading since 1981 while Eurozone inflation registered 8.1% and UK inflation hit a new multi-decade high of 9.1%.

Global equities experienced another turbulent month as all major developed markets ended lower. The S&P 500 fell 8.3% in June and recorded its largest first-half contraction since 1970. Emerging Markets were relatively stronger over the month as the easing of COVID-19 restrictions helped Chinese equities move higher in June.

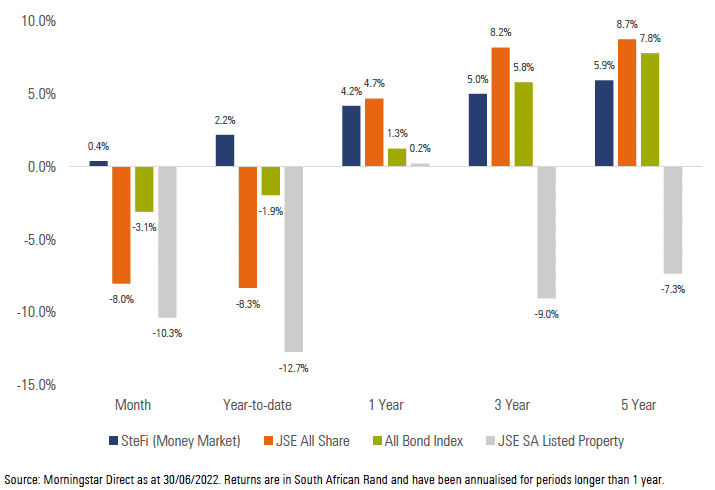

Exhibit 1: SA Market Performance (total returns)

All major SA asset classes were under pressure over June with only cash generating a marginally positive return over the month. Foreigners remained net sellers of both SA equities and bonds while the rand ended the month around 4.1% weaker against the US Dollar after breaking through some resistance at R16/$.

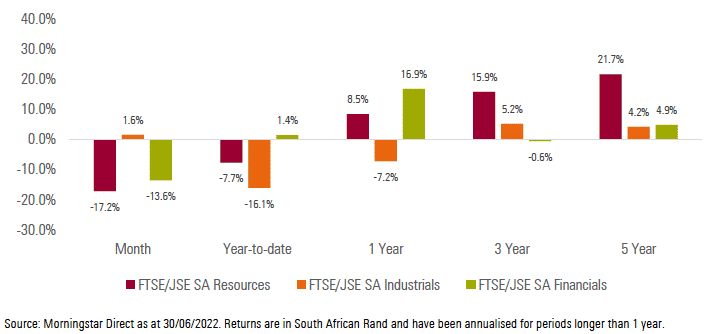

South African equities were down as the Resources and Financials sectors came under significant selling pressure. All the main commercial banks and insurers were down by more than 10% over the month while the leading materials companies gave back much of their gains from the start of the year. Industrials also struggled but were rescued by the re-rating of Naspers and Prosus following the announcement of an open-ended buyback programme through the intended unwinding of their holding in Tencent.

Local bonds were also not spared and were weaker over the month after posting positive returns in May. Yields on the benchmark 10-year SA government bond moved close to 11% as pressure in global fixed income markets, as well as uncertainty around the domestic outlook for inflation, continued to concern both local and foreign investors. Inflation-linked bonds faired relatively better but were also down over the month.

Local listed property had an especially challenging month and continues to trend lower as inflation and bond yields move higher.

Local inflation increased to 6.5% (year-on-year to the end of May) and moved through the upper limit of the Reserve Banks’ 3% – 6% target band. Food and transport were the main contributors to the higher print with these costs expected to continue to apply upward pressure on inflation given the fallout from the ongoing Russian invasion of Ukraine.

SA consumer confidence, as measured by the FNB/BER Consumer Confidence Index (“CCI”) dropped to its lowest level since June 2020. Excluding the COVID-19-induced Level 5 lockdown period during the initial outbreak of the pandemic in South Africa, the CCI is currently at its lowest level since 1986.

SA growth still faces significant challenges as higher global interest rates and inflation adversely affect growth prospects but there was also some good news over the month. Stats SA reported that growth for the first quarter of the year came in ahead of expectations at 1.9%. The country also continues to benefit from a strong trade surplus, as the amount by which exports exceed imports increased to over R28bn in May from a revised R16bn the previous month.

Exhibit 2: SA Sector Performance (total returns)

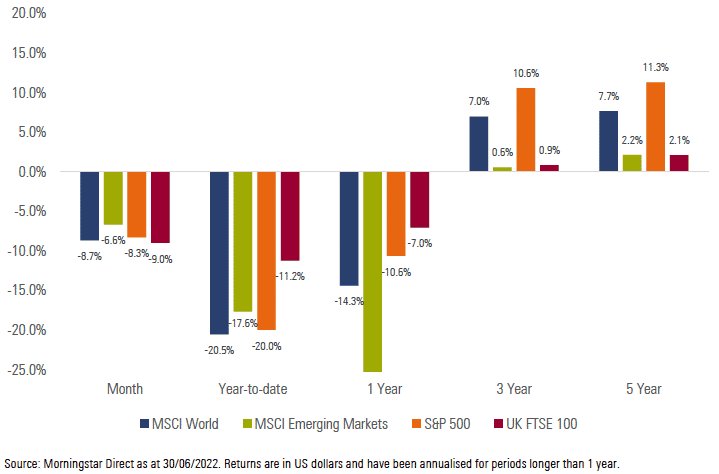

Most of the major developed equity markets ended the month in negative territory. The MSCI World Index delivered a return of -8.6% for the month.

Emerging market equities fared slightly better than developed markets, Chinese equities propped up the performance of the sector. The MSCI Emerging Markets Index delivered a return of -6.6% for the month.

Most of the major global equity markets were down for the month after concerns around global growth become front of mind for investors. The UK’s FTSE 100 (-9.0%), Germany’s FSE DAX (-13.3%) and Japan’s Nikkei 225 (-8.2%) all delivered negative performance for the month. China’s Shanghai SE Composite (+6.1%), which has been under significant pressure on a year-to-date basis, experienced a positive turnaround over the month.

US equities set the trend for developed markets. The S&P 500 (-8.3%) and NASDAQ 100 (-8.9%) continued to fall as technology companies’ growth and earnings expectations came under persistent investor scrutiny.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios struggled to generate positive performance over the month. This was largely due to weak performance from risk assets including equities and listed property. Rand weakness over the month did provide a tailwind to the performance of global asset classes, however, this was largely insufficient to compensate for negative hard currency returns from major global equity markets.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation-driven approach by allocating assets to the most attractive areas of the market from a reward-for-risk perspective. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

Market summary

Click on the link below to download June’s market summary.