Global equity markets experienced a challenging start to the year, posting their worst performance for January since 2016. Market sentiment was weighed down by concerns around higher inflation, hawkish rhetoric from central banks and growing tensions at the Ukrainian border with Russia.

Global bonds also continued to struggle in the month of January. The asset class delivered its worst start to the year since 2009 against a backdrop of elevated inflation and investors positioning their portfolios for higher interest rates.

The US Federal Reserve (Fed) released its December FOMC minutes early in January and they were more hawkish than expected. The minutes indicated that many participants on the committee believed a rate hike may be appropriate sooner than previously expected. Participants also indicated that rate hikes may proceed at a faster pace than had been previously anticipated, and some members suggested it could be appropriate to start the process of quantitative tightening soon after the first interest rate hike.

The Fed meeting that followed later in the month suggested a confirmation of the hawkish tone expressed in the December minutes. January’s FOMC statement signalled that the rate hiking cycle could potentially begin in March, as opposed to prior expectations of a lift-off in June.

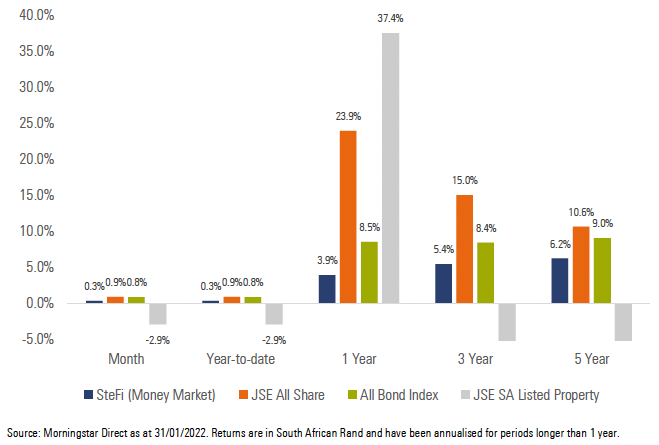

Exhibit 1: SA Market Performance (total returns)

South African equities ended the month in positive territory, outperforming other developed and emerging markets on the back of strong performance from financials and commodity counters.

Local bonds also had a positive month despite December’s inflation coming in higher than expected. Their performance was supported by the relatively attractive yields on offer, which remain above the middle of the inflation target.

Local listed Property had a volatile month and ended January in negative territory. The large index constituents had negative performance as the hawkish rhetoric from global central banks affected market sentiment.

The rand had positive performance against major developed market currencies over the month, strengthening against the US dollar, the euro and the pound sterling.

SA headline CPI increased to 5.9% year-on-year for December (from 5.5% in November). The largest contributor to the increase in headline CPI was transport, driven by rising petrol and diesel prices. Higher prices in food and non-alcoholic categories also contributed to the increase in inflation.

The South African Reserve Bank (SARB) increased the repo rate by 25bp to 4% in January and revised its inflation forecast for 2022 from 4.3% to 4.9%. The SARB also revised its economic growth forecast for 2021 from 5.2% to 4.8% to account for the contraction during the third quarter of 2021 caused by the Omicron Covid-19 variant-led disruptions.

SA’s trade surplus narrowed in December to R30.14 billion, from a surplus in November of R35.8 billion.

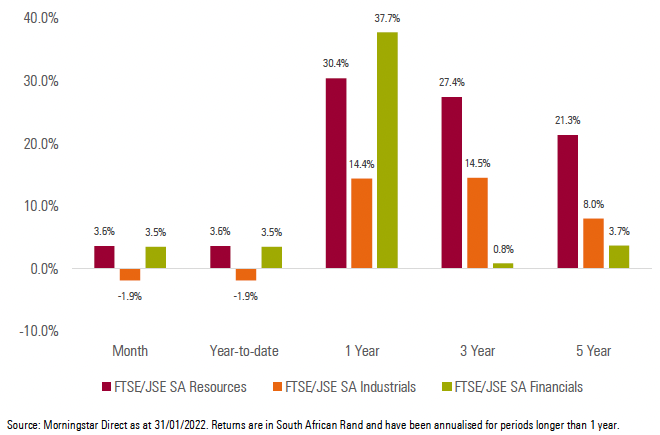

Local equity sectors were led by strong performance from Financials (+3.5%) and Resources (+3.6%), while Industrials (-1.9%) ended the month lower.

Exhibit 2: SA Sector Performance (total returns)

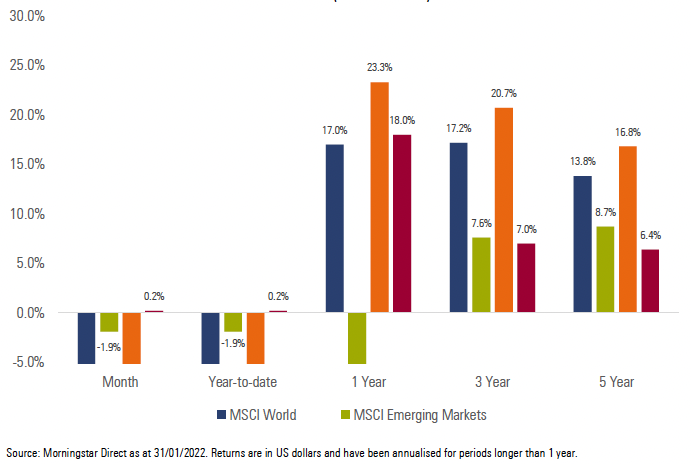

Most of the major developed equity markets ended the month lower, amid concerns of persistently elevated inflation and potentially higher interest rates in major developed markets. The MSCI World Index delivered a return of -5.3% for the month.

Despite outperforming developed markets, emerging market equities also delivered negative performance. The MSCI Emerging Markets Index delivered a return of -1.9% for the month

Most of the major equity markets ended the month in negative territory. Germany’s FSE DAX (-4%), Japan’s Nikkei 225 (-6.3%) and China’s Shanghai SE Composite (-7.5%) all delivered negative performance for the month, while the UK’s FTSE 100 (+0.2%) was largely flat.

US equities also delivered negative performance, with the technology-heavy NASDAQ 100 (+8.5%) ending the month in deeper negative territory than the S&P 500 (-5.2%).

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios generated negative returns over the month. This was largely driven by the sell-off in global markets on the back of a hawkish Fed, an increase in the expectation of faster rate hikes and continuous geopolitical tension. The sell-off in global equities were partially offset by modest gains in local equities mainly driven by resources and financials. Those portfolios with an income focus managed to generate decent returns over the month, largely due to strong performance from medium and long-dated SA bonds.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation driven approach by allocating assets to the most attractive areas of the market from a reward for risk perspective. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio, independent of the prevailing market environment.

Market summary

Click on the link below to download January’s market summary.