Most major equity markets managed to end the month in positive territory, despite significant volatility in global bond markets towards the end of February amid concerns of rising inflation expectations and possible future interest rate moves.

Markets were driven higher during the month by strong Q4 2020 company earnings announcements and positive news on vaccine rollouts, with the US approving the Johnson and Johnson vaccine on 28 February.

There was also progress on a new US stimulus package, with a $1.9 trillion Covid relief bill passed by the US House of Representatives, following which it will be considered by the US Senate.

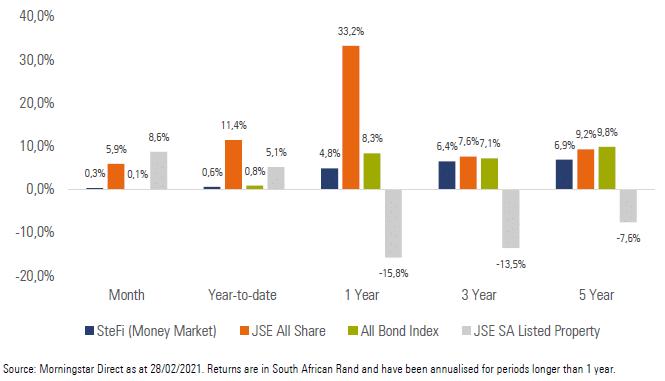

Exhibit 1: SA Market Performance (total returns)

South African equities ended higher for a fourth consecutive month, driven largely by strong performance from large cap resource counters on the back of significant positive commodity price moves.

Local bonds ended the month with flat performance, despite developed market sovereign bonds selling off significantly during February and ending with their worst monthly performance in over 35 years.

Local listed property ended the month with strong performance in line with other SA risk assets, as investors looked forward to a resumption of economic activity amid declining Covid-19 cases in the country.

The rand was broadly unchanged against most major developed market currencies, despite significant volatility during the month in connection with the budget speech as well as global bond yield movements.

On 24 February, Finance Minister Tito Mboweni tabled the 2021/2022 Budget in Parliament. The minister announced that revenue is expected to be around R100 billion ahead of expectations, largely due to tax collections from the mining sector coming in higher than expected due to booming commodity prices, coupled with a recovery in VAT.

While the country’s debt burden remains unsustainable, the moves by National Treasury to cancel a proposed R40 billion in tax hikes over the next four years and above inflation increases in personal income tax brackets will be welcomed by local citizens.

South African President Cyril Ramaphosa announced on 28 February that the country will move to a level 1 lockdown, to aid a resumption of economic activity amid declining daily Covid-19 cases.

SA headline CPI moved higher to a year-on-year figure of 3.2% for January (from 3.1% in December), with increases in fuel, food and non-alcoholic beverages being the largest contributors to the move.

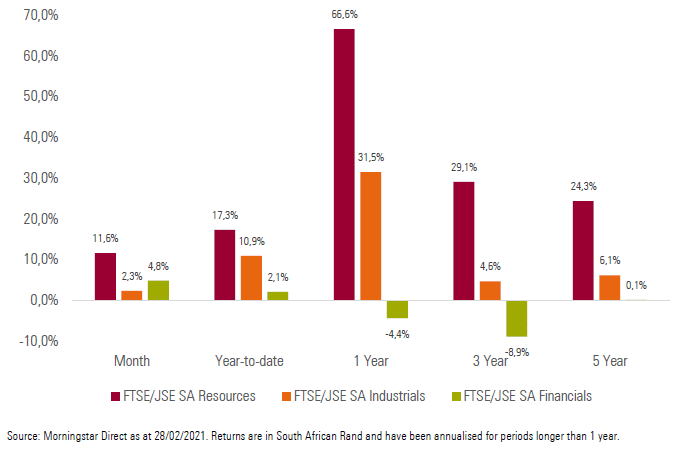

All local equity sectors ended the month higher, with Resources (+11.6%), Financials (+4.8%) and Industrials (+2.3%) finishing the month with positive returns.

Exhibit 2: SA Sector Performance (total returns)

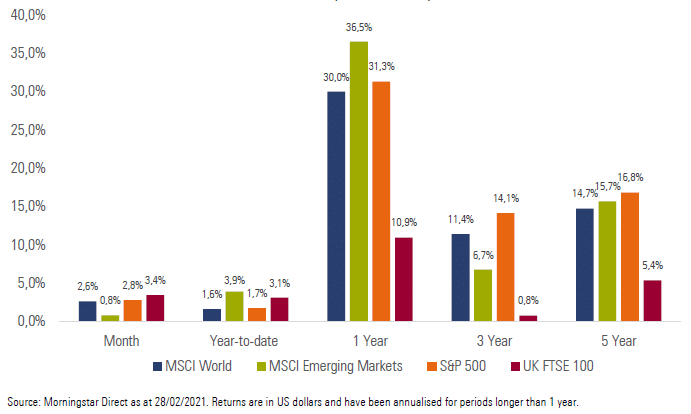

Most major developed equity markets ended the month with positive returns, despite selling off slightly towards the end of February. The MSCI World Index delivered a return of +2.6% for the month.

Emerging market equities underperformed developed markets over the month, despite ending February in the green. The MSCI Emerging Markets Index delivered a return of +0.8% for the month.

Major equity markets ended the month higher, with the UK’s FTSE 100 (+3.4%), Japan’s Nikkei 225 (+2.9%), Germany’s FSE DAX (+2.5%) and China’s Shanghai SE Composite (+0.8%) all ending the month higher.

US equities had mixed performance for the month, with the S&P 500 (+2.8%) ending the month higher and the tech heavy NASDAQ 100 (-0.0%) ending the month largely flat, weighed down by poor performance from technology counters towards the end of February.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios managed to deliver strong performance for the month, particularly those with significant allocations to SA risk assets. Global equity allocations also drove performance over the month, particularly allocations to more cyclical areas of the market, including energy and financials. Income focused investors faced a dual headwind from flat performance from the SA bond market as well as negative performance from offshore developed sovereign bond markets. Despite this, most income focused portfolios managed to eke out positive returns for the month.

We are pleased with returns generated by portfolios so far this year, particularly the positive contribution from SA equities after a lengthy period of disappointing performance. This serves to remind us that as a small emerging economy, the performance of SA equities is often at the mercy of global sentiment and risk taking. Over and above this, many of the large counters listed on JSE earn significant amounts in offshore markets and are therefore not reliant on the SA economy to perform. We will continue to seek to allocate capital using our valuation driven approach, relying on the three pillars of asset allocation, manager selection and portfolio construction to deliver strong absolute and relative returns at lower levels of risk.

Market summary

Click on the link below to download February’s market summary.