Global equity markets delivered strong performance in December, supported by the continuation of the global economic recovery, as the Omicron variant of Covid-19 appears to be resulting in less hospitalisations and deaths than previous variants, despite causing significant disruptions.

Global bond markets battled to come to terms with persistently elevated inflation, with the asset class delivering negative performance for the 2021 calendar year (the first time since 1999) amid concerns of higher interest rates in major developed markets.

The US Federal Reserve (Fed) outlined plans at its December meeting to double the pace at which it tapers asset purchases, which would effectively result in the Fed withdrawing its Covid-19 induced $120 billion per month bond-buying programme more rapidly.

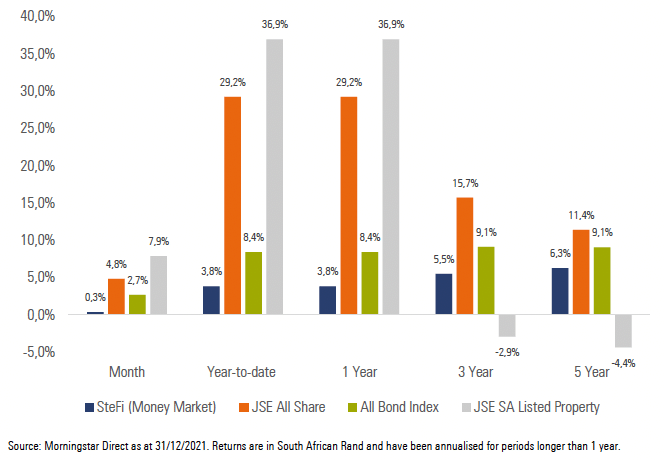

Exhibit 1: SA Market Performance (total returns)

South African equities delivered strong performance for December, outperforming other emerging equity markets over the month, supported by the performance of large cap Resource counters.

Local bonds had a strong month, supported by the performance of medium and long dated instruments which recovered significantly post the initial concerns around the Omicron Covid-19 variant.

Local listed property also delivered strong returns, supported by the performance of large index constituents and the continuation of level 1 lockdown restrictions (and some easing of lockdown measures) during December, which proved supportive of sentiment towards the asset class.

The rand had mixed performance against major developed market currencies over the month, ending largely flat against the US dollar and the euro and slightly lower against the pound sterling.

In terms of the Covid-19 pandemic, it appears that SA has passed the peak of the fourth wave of infections, with the government lifting the curfew in place from 12am to 4am, resulting in no further restrictions on the movement of SA citizens.

SA real GDP slumped in Q3 2021 by -1.5% after recording four consecutive quarters of growth, which impacted the recovery that the country has made since the initial Covid-19 induced lockdown in the second quarter of 2020.

SA headline CPI increased to 5.5% year-on-year for November (from 5.0% in October). The increase in headline CPI was largely a result of higher fuel prices, while food prices moderated slightly over the month.

SA’s trade surplus widened in November to R35.8 billion, from a revised surplus in October of R2.7 billion.

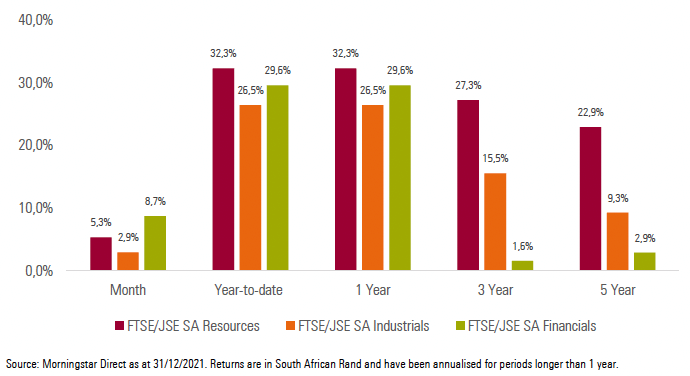

Local equity sectors all ended the month higher, with Financials (+8.7%), Resources (+5.3%) and Industrials (+2.9%) all delivering strong performance.

Exhibit 2: SA Sector Performance (total returns)

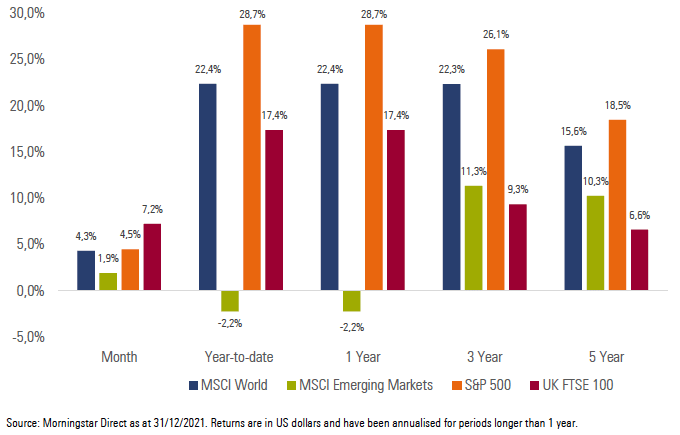

Most of the major developed equity markets ended the month higher, as concerns around the Omicron Covid-19 variant receded during the month. The MSCI World Index delivered a return of +4.3% for the month.

Emerging market equities also delivered positive performance, despite underperforming developed equity markets slightly over the month. The MSCI Emerging Markets Index delivered a return of +1.9% for the month.

Most of the major equity markets ended the month in positive territory. The UK’s FTSE 100 (+7.2%), Germany’s FSE DAX (+6.3%), Japan’s Nikkei 225 (+2.2%) and China’s Shanghai SE Composite (+2.1%) all delivered positive performance for the month.

US equities also delivered positive performance, with the S&P 500 (+4.5%) outperforming the technology heavy NASDAQ 100 (+1.2%) slightly over the month.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios managed to generate strong returns over the month. This was largely driven by the performance of local and global risk assets including equities and listed property. Those portfolios with an income focus managed to generate decent returns over the month, largely due to strong performance from medium and long dated SA bonds.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation driven approach by allocating assets to the most attractive areas of the market from a reward for risk perspective. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

Market summary

Click on the link below to download December’s market summary.