We were all excited to see the end of 2020 and yet I doubt we thought we would be spending it in lockdown. It was a remarkable year that saw many landmark changes, including the finalisation of Brexit. While history books will be littered with notable events, when it comes to money matters, a stand-out from 2020 will be the disconnect between devastated economies and rampant markets. A second interesting point worth noting is the divergence of returns within markets, with only a handful of shares and sectors driving broad market returns, while most shares ended the year either flat or in negative territory. It was the eye watering returns from select shares in South Africa and abroad that were responsible for the overall positive level of markets.

Global markets continued to climb higher in December, supported by the start of Covid-19 vaccinations in many countries, despite concerns around an increase in infection rates as well as the development of a new virulent strain.

The anticipated announcement of a $900 billion stimulus package in the United States as well as the finalisation of a Brexit deal between the United Kingdom and the European Union also drove the risk-on sentiment.

The US Federal Reserve (Fed) announced subsequent to its meeting in December that it will continue to buy at least $120 billion of bonds every month until the US economy reaches full employment and inflation stays at 2%. It also voted to keep interest rates close to zero, supporting the lower interest rates for longer narrative.

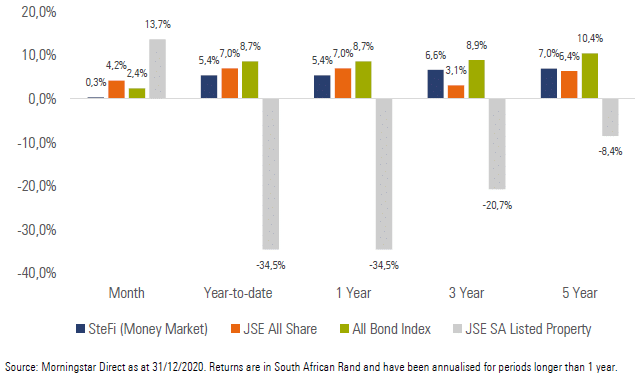

Exhibit 1: SA Market Performance (total returns)

South African equities ended the month higher, in line with the positive moves in global markets, largely driven by strong performance from both Financials and Resources.

Local bonds also continued to deliver strong performance during the month, supported by the continuation of foreign buying (foreigners bought R19.8 billion of local bonds in December) and a contraction in the SA sovereign credit spread which pushed yields lower. It is good to see foreign appetite returning for SA bonds which have been shunned by foreign investors for many years.

Despite ending the year in double digit negative territory, local listed property continued its recent rebound, as market participants took advantage of the risk on environment to allocate more to this out of favour area of the market.

The rand was stronger against most major currencies for the month, supported by net purchases of SA equities and bonds by foreigners and a continuation in the SA trade surplus. Who would have thought the rand would end the year around R14.70, having reached a high (or low should we say) of close to R19.00 to the US dollar.

South African President Cyril Ramaphosa announced the move to an “adjusted level 3” lockdown during the month, as Covid-19 infection rates picked up across the country, particularly in Kwazulu-Natal, the Western Cape and Gauteng.

Following the sharp recovery in economic growth in the third quarter of 2020, economic data appears to indicate that activity post the nationwide lockdown in Q2 continues to normalise, however, there is a concern that the impact of a slower than expected holiday season as well as the tighter lockdown restrictions may impact growth going forward.

SA’s trade surplus continued to be resilient, with strong export figures leading to a trade surplus of R37 billion for November (following a restated figure of R35 billion for October). The strength in the trade surplus is evident in the year-to-date figure for 2020 of R238 billion (to the end of November), compared to the figure of R9 billion for the same period in 2019.

SA headline CPI eased to a year-on-year figure of 3.2% to the end of November (from 3.3% in October), despite higher food inflation continuing to put upward pressure on the rate of inflation.

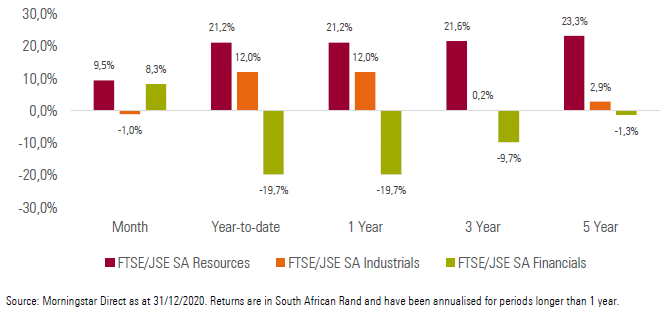

The performance of local equity sectors was mixed, with Resources (+9.5%) and Financials (+8.3%) ending the month sharply higher, while Industrials (-1.0%) fared slightly worse.

Exhibit 2: SA Sector Performance (total returns)

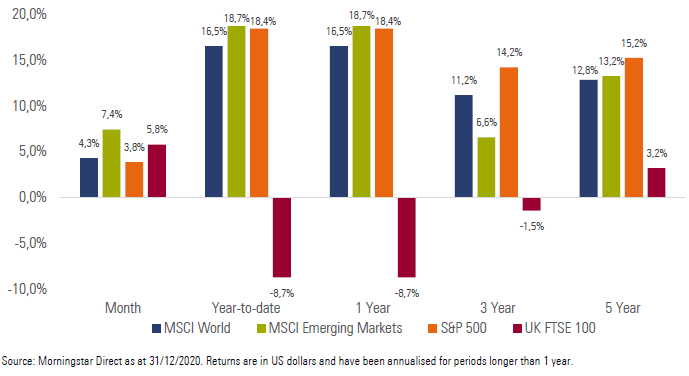

Most major developed equity markets ended the month higher, supported by the rollout of Covid- 19 vaccines in some countries as well as the $900 billion stimulus package announced in the United States. The MSCI World Index delivered a return of +4.3% for the month.

Emerging market equities also delivered strong performance for the month, outperforming developed markets slightly. The MSCI Emerging Markets Index delivered a return of +7.4% for the month.

All major equity markets ended the month higher, with the UK’s FTSE 100 (+5.8%), Germany’s FSE DAX (+5.6%), Japan’s Nikkei 225 (+5.0%) and China’s Shanghai SE Composite (+3.1%) all delivering strong performance for the month.

US equities also ended the month higher, with both the tech heavy NASDAQ 100 (+5.1%) and the S&P 500 (+3.8%) ending the month with decent performance.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios managed to end the year on a strong note, supported by decent returns from all local asset classes. In a continuation of the recent trend, the rand acted as a slight headwind to the performance of global allocations, as it strengthened against most major developed market currencies over the month. Income focused investors also generated decent returns for the month, supported by strong positive moves in the local bond market as foreigners continued to be net buyers of SA bonds during the month.

While most markets ended the year in positive territory, it was a challenging year for money managers as the majority of shares declined and positive market returns were driven by a handful of shares and sectors – both in SA and globally. We are pleased by the returns generated by portfolios for the 2020 calendar year. While the announcements and rollout of Covid vaccines are encouraging, we would expect markets to remain sensitive to news flow until global infections are under control. As always, investors need to focus on what they can control, investing for the long-term and avoiding behaviour which will impede them from achieving their long-term financial goals.

Market summary

Click on the link below to download December’s market summary.