Global markets experienced a volatile August and ended the month lower. Investors turned their focus to the hawkish comments received from the US Federal Reserve’s Jerome Powell at the Jackson Hole Economic Symposium. Concerns surrounding higher interest rates for longer to tame inflation exacerbated worries about possible recessions and a slower growth environment. This led to a period of risk-off sentiment, leading global markets lower, particularly towards the second half of August. Many global equity markets erased the strong gains recorded at the beginning of the month.

Global inflation prints continue to remain elevated. The annual inflation rate in the US slowed to 8.5% (year-on-year to the end of July), which was below market consensus of 8.7%. Whilst in the UK, inflation increased to 10.1% (year-on-year to the end of July), ahead of market expectations and the highest reading since 1982. The annual inflation rate in the EU increased to 9.1% in July of 2022, which is a new record high and continues to be driven primarily by energy costs, which have risen by 38.3% over the past year.

During its August meeting, the Bank of England raised interest rates by 0.5% to combat persistently high inflation. This is the sixth consecutive, and most significant rate hike since 1995. In an opposite pattern, the People’s Bank of China lowered its key loan prime rates to revive borrowing demand and combat the continued economic pressures posed by the prevailing COVID-19 lockdowns in China. The 1-year loan prime rate (LPR) was lowered by 0.05% to 3.65% (to a record low), whereas the 5-year LPR was lowered by 0.15% to 4.3%.

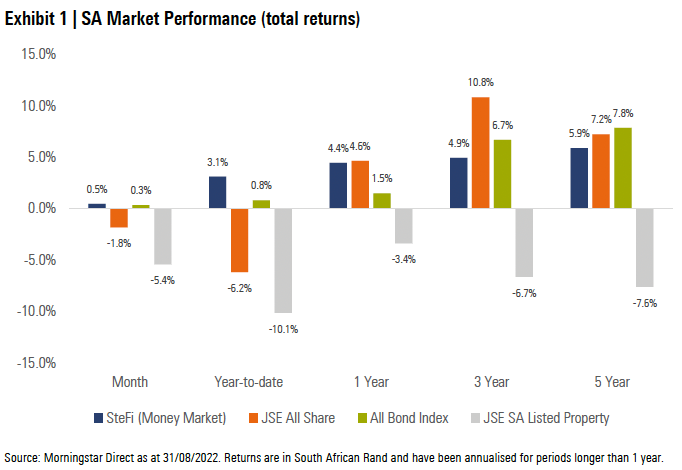

Exhibit 1: SA Market Performance (total returns)

Most South African asset classes followed their global peers lower in August, as markets reversed the early month gains to post a negative return.

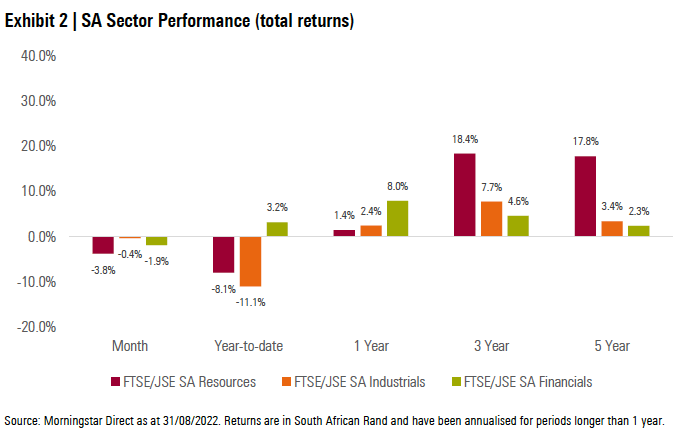

South African equities ended August in the red, with all sectors posting negative returns. Resources were the biggest laggard, on the back of weaker commodity prices as a result of slowing global growth. Financials also trended lower, as insurers came under pressure due to the Competition Commission raid on their offices for suspected collusion. Industrials were more resilient and produced a respectable (albeit negative) return given the more significant decline in equity markets.

Local bonds ended the month higher and fared better than developed markets peers. The yield curve shifted higher by the end of August, driven largely by the selloff in 10yr US treasuries, a strong US dollar, and the global risk off environment.

Property had a tough month as inflation and bond yields moved higher. Listed property was the worst performing asset class for the month of August. Large index constituents including Redefine and Fortress fell significantly over the month.

South Africa’s SACCI business confidence index rose to 110.3 last month (year-over-year to the end of July). It was the highest reading since March, helped by increased trade volumes and new vehicle sales. Despite the improvement in business confidence, price pressures and a volatile rand exchange rate, together with higher interest rates continued to weigh on the local business environment.

The local inflation rate increased to an over 13-year high of 7.8% (year-on-year to the end of July), above market expectations of 7.7% and the upper limit of the South African Reserve Bank’s target range of 3%-6%. Transport prices, mainly comprised of fuels, continued to be the main driver of local inflation.

South Africa’s unemployment rate fell to 33.9% in Q2 of 2022, below the record high of 35.3% set in Q4 of 2021. The expanded definition of unemployment (which includes members of the public who are no longer seeking employment) was at 44.1%, down from 45.5% in the first quarter. The youth unemployment rate, measuring jobseekers between 15 and 24 years old, fell to 61.4% in the second quarter of 2022, the lowest in almost two years.

Exhibit 2: SA Sector Performance (total returns)

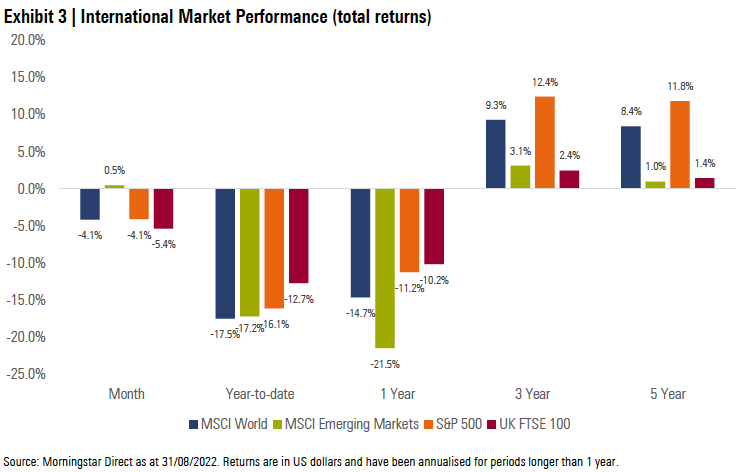

Most of the major developed equity markets ended the month in negative territory after a rebound in July. The MSCI World Index delivered a return of -4.1% in August, lagging its emerging market peers.

Emerging market equities outperformed developed market equities. The MSCI Emerging Markets Index ended the month up +0.5%.

Most of the major global equity markets fell strongly after the July rebound and ended the month of August in negative territory. The UK’s FTSE 100 (-5.4%), Germany’s FSE DAX (-6.1%) and Japan’s Nikkei 225 (-2.5%) all delivered negative performance for the month. China’s Shanghai SE Composite (-3.8%) continued to come under pressure in August.

US equities had a volatile month. After rising strongly in the first half of August, the US equity market ended significantly down as of the end of August. The S&P 500 (-4.1%) fell sharply along with the technology-heavy NASDAQ 100 (-5.1%).

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Following positive performance in July, markets reversed course in August and most portfolios struggled to generate meaningful performance over the month. This was largely due to a selloff in risk assets including equities and listed property. Rand weakness over the month did provide a tailwind to the performance of global asset classes, however, this was largely insufficient to compensate for negative hard currency returns from major global equity markets.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We are reminded that economic events such as possible recessions and the uncertainties that come with them bring out behavioural biases and focus investors on the short term. We will continue to follow our valuation driven approach by allocating assets to the most attractive areas of the market from a reward for risk perspective and ensure we build robust portfolios. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

Market summary

Click on the link below to download August’s market summary.