The main purpose of a retirement fund is simple: to build up enough savings during your working years so that you are able to continue living the lifestyle you have become accustomed to when you retire. Retirement planning is therefore the simple concept of planning financially for the day you retire. Life, however, does not always go as planned.

It’s important to understand what happens to your employer-provided retirement fund benefits in the event of your untimely death. If you are a member of a retirement fund, you will have a retirement savings account, and these accumulated savings will be paid out to your nominees or beneficiaries when you die. Over and above the retirement savings, you may have a lump-sum death benefit, which will either be an approved or an unapproved benefit.

The Pension Funds Act allows for the provision of lump-sum death and disability benefits as approved benefits. But these benefits can also be provided as unapproved benefits. The difference between these two types of death benefits is often misunderstood by fund members. Research by Momentum Corporate on members’ understanding of terminology used across the employee benefits sector revealed that members are uncomfortable with these two terms.

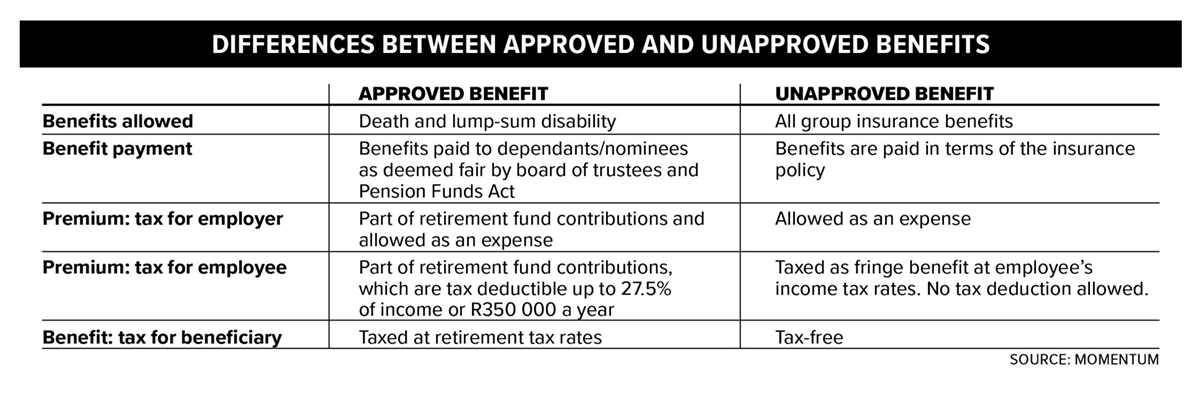

Approved benefits are provided through your retirement fund, whereas unapproved benefits are provided through a separate employer policy. Because different rules and regulations apply to the distribution and payment of the approved and unapproved benefits, it is important to know which type you have and the implications this will have on how the lump sum is distributed to your nominees or beneficiaries. There are also other differences between approved and unapproved benefits, such as tax treatment (see table at end of this article).

Approved lump-sum death benefit

An approved lump-sum death benefit is provided through a retirement fund. This means that the retirement fund is the policyholder and the same rules apply as for the retirement savings account balance.

When a member dies, the trustees of the retirement fund will decide who will receive the benefits, what portion of the benefit they will receive, and how it should be paid, using the member’s beneficiary nomination form and the Pension Funds Act as a guideline. Your dependants will be considered first, followed by your non-dependant nominees.

In the case of an approved benefit, an employer has no say over the distribution and payment of the benefit. The trustees, however, can ask the employer for information during the decision-making process.

It is important to note that your wishes as stipulated in your will and testament cannot override the trustees’ decision in this regard.

Unapproved lump-sum death benefit

An unapproved benefit is provided outside of the retirement fund – and therefore isn’t subject to the Pension Funds Act.

Also known as a stand-alone death benefit, an unapproved benefit is provided through a separate insurance policy that the employer took out for the members. This means that the employer is the policyholder and must make sure that the member’s benefits are distributed according to the policy rules.

With an unapproved benefit, your beneficiary nomination form will be followed as long as it is in line with the policy rules, and the trustees have no say over the distribution and payment of this benefit.

That said, as is the case for approved lump-sum benefits, your wishes as stipulated in your will and testament cannot override the policy rule. This is why it’s important to ensure that if you are a member of an employer-sponsored retirement fund, you fill out the beneficiary nomination form, where you nominate dependants and nominees. This will help guide the trustees or the employer with the distribution of the benefits.

If you are unsure of which type of benefit you have, you should check your benefit statements. If your employer has taken out stand-alone insurance cover, these (unapproved) benefits will not show on your retirement fund benefit statement. In this case, you will need to obtain information about these benefits from your employer by consulting your human resources officer.

Seek advice

It’s important to seek advice from a financial adviser or to get an understanding of your retirement benefit options through retirement benefits counselling – a service which is accessible via your retirement fund. Having a long-term relationship with a professional financial adviser who will offer appropriate advice is paramount to reaching your financial goals and ensuring that your dependants are taken care of in the event of death.

Finally, it’s important to keep beneficiary information up to date. Outdated or missing beneficiary nomination forms are very often the reason for lengthy delays in the payment of a death benefit – a time when the member’s dependants are often in financial need.

As circumstances change from time to time, it is crucial to regularly update your beneficiaries’ information so that the benefits can be paid to the right people without any unnecessary delay.

This article first appeared in Personal Finance