Global markets endured another volatile month as the effects of higher inflation, rising interest rates, continued geopolitical instability and the looming threat of a potential global recession continued to weigh on investor sentiment and asset prices.

Both US and global markets experienced wild swings, as assets continued to sell off heavily in the first half of May, before staging a late recovery towards the end of the month. There was some reprieve for emerging markets. The Chinese government announced an easing of lockdown restrictions after months of its zero-COVID strategy weighing negatively on both the real economy and financial markets. Chinese equities experienced a month-end rally, with both the Hang Seng and Shanghai Composite moving positive after an especially difficult start to the year.

The US Federal Reserve increased interest rates by 0.5% at their meeting in early May. Global inflation remains stubbornly high, with the US inflation print coming in at 8.3% (year-on-year to the end of April), Eurozone inflation registering a higher-than-expected 8.1%, and UK inflation also hitting a multi-decade high of 9%. The Russian invasion of Ukraine continues to put upward pressure on global energy and food prices, with global supply chain issues further exacerbating the largely unprecedented levels of inflation being seen around the world.

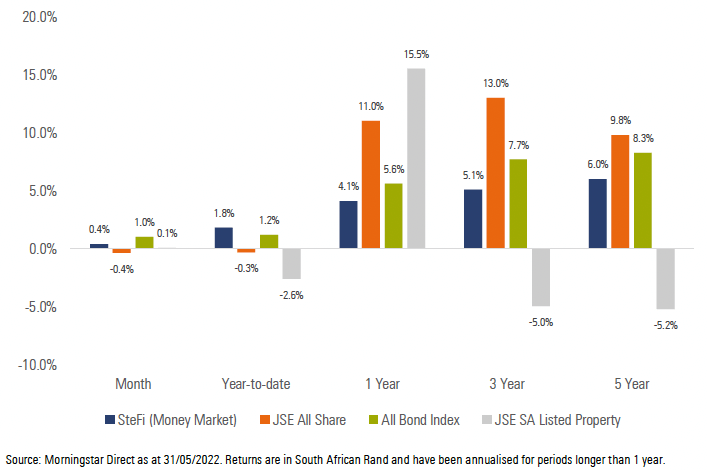

Exhibit 1: SA Market Performance (total returns)

South African equities were relatively flat over the month, with banking and insurance stocks, which are relatively more resilient to rising interest rates, recovering from an especially weak April.

Local bonds were the best performing domestic asset class after experiencing some selling pressure in April. Inflation-linked bonds performed especially well as the market continues to price in the probability of potentially higher-than-expected local and global inflation. Demand for local bonds was mostly from SA investors as foreigners remained net sellers in May. Local listed property traded relatively flat, with no significant moves from SA REIT’s over the month.

The rand remains especially volatile, but the currency retraced some of the losses against some of the major developed market currencies over the month. Rand gains were more attributable to broader US dollar weakness as the greenback dropped off from 52-week highs towards month end. Local inflation remained unchanged at 5.9% (year-on-year to the end of April), with fuel and food prices lower than the previous prints but continuing to put pressure on headline inflation. South Africa remains one of only a few emerging markets where inflation is coming in within the target band range.

The South African Reserve Bank’s (SARB) Monetary Policy Committee increased the repo rate by 0.5% to 4.75%. This was the largest hike since 2014. The decision to hike was unanimous, with only one of the five MPC committee members voting for a lower 0.25% increase.

South Africa’s unemployment rate declined slightly over the first quarter of the year, coming in at 34.5% versus 35.3% in the previous quarter. Unemployment remains much higher than it should be, but this was the first decline in almost 2 years.

In other positive news, global credit rating agency, S&P upgraded its outlook on SA from stable to positive with the country rating remaining at BB-/B. This follows the Moody’s upgrade from negative to stable in April.

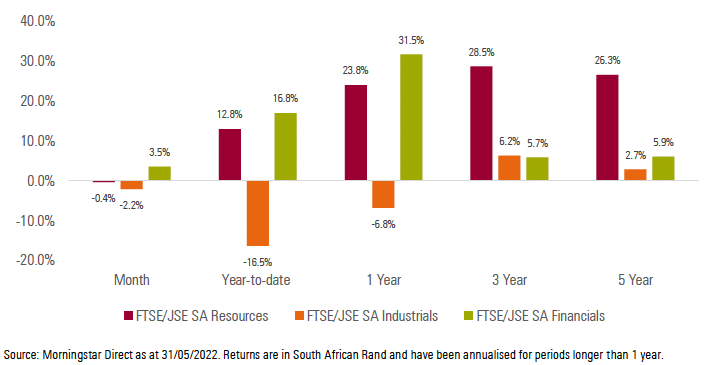

Resources (-0.4%) and Industrials (-2.2%) continued to experience selling pressure over the month while Financials (+3.5%) recovered after being down in April. All the major banks including Nedbank (+7.1%), Absa (+6.9%), Investec (+6.8%), Standard Bank (+6.4%) and FirstRand (+5.7%) were top 10 market performers over the month.

Exhibit 2: SA Sector Performance (total returns)

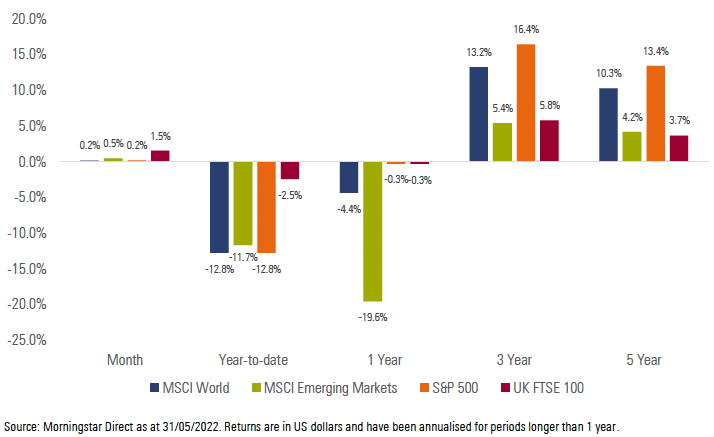

Most of the major developed equity markets ended the month in positive territory, after enduring a tough start to the month and rebounding towards month end. The MSCI World Index delivered a return of +0.2% for the month.

Emerging market equities experienced some much need respite, after the decline in Chinese equities stemmed in May. The MSCI Emerging Markets Index delivered a return of +0.5% for the month.

Most of the major global equity markets enjoyed a slight rebound after a difficult April and ended the month in positive territory. The UK’s FTSE 100 (+1.5%), Germany’s FSE DAX (+3.6%) and Japan’s Nikkei 225 (+2.3%) all delivered positive performance for the month. China’s Shanghai SE Composite (+3.5%), which has been under significant pressure on a year-to-date basis, also experienced a positive turnaround over the month.

US equities had mixed fortunes over the month. The S&P 500 (+0.2%) moved slightly higher while the NASDAQ 100 (-1.5%) continued to fall as technology companies’ growth and earnings expectations came under persistent investor scrutiny.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios struggled to generate meaningful returns over the month. This was largely driven by flat performance from risk assets including SA equity and property as well as global equities. The rand acted as a slight headwind to the performance of offshore assets over the month, ending marginally stronger against most major developed market currencies. Income focussed investors managed to generate decent returns over the month, as local nominal bonds and inflation linked bonds delivered positive returns over the month.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation driven approach by allocating assets to the most attractive areas of the market from a reward for risk perspective. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

Market summary

Click on the link below to download May’s market summary.