April proved to be a tough month for global equity markets, with the bulk of the major global markets ending the month with negative returns. Markets were weighed down by continued concerns around Russia’s war in Ukraine, inflationary pressures (and the possibility of higher interest rates) as well as China’s restrictions on the movement of citizens to curb rising Covid-19 infections.

The weak performance from global equity markets was most pronounced in the US, with the technology heavy NASDAQ 100 coming under pressure on the back of disappointing results from Apple as well as Amazon reporting its first net loss since 2015 and the slowest sales growth in its e-commerce business in two decades.

Inflation continued to climb higher in the US, with March year-on-year headline inflation coming in at 8.5% (the highest in three decades). Markets now expect the US Federal Reserve to move interest rates higher by 0.50% at their meeting in early May.

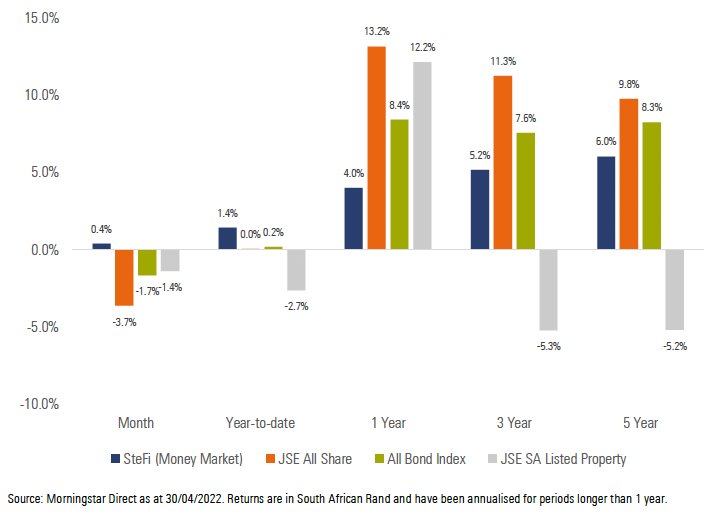

Exhibit 1: SA Market Performance (total returns)

South African equities tracked global markets lower during the month, weighed down by weak performance from all local equity sectors, particularly those in the banking and insurance sectors.

Local bonds remained under pressure during the month, as the global risk off environment and renewed concerns around lacklustre SA GDP growth led to higher yields (and lower prices). Local listed property also ended the month lower, as poor performance from large index constituents including Redefine, Resilient and Growthpoint acted as a headwind to the performance of the asset class.

The rand reversed course during April, giving back a significant portion of its recent gains against the major developed market currencies. A strong US dollar, continued loadshedding by Eskom and flood damage in KwaZulu-Natal and the Eastern Cape which led to the government declaring a national state of disaster all weighed on the performance of the rand.

KwaZulu-Natal (KZN) was heavily impacted by flooding during the month, as the government declared a national state of disaster on the back of the destruction of key infrastructure, which left close to 40,000 people homeless.

SA headline CPI increased to 5.9% year-on-year for March (from 5.7% in February). The increase in headline CPI was largely a result of the transport category of the CPI basket, which was impacted by higher oil prices.

South Africa’s trade surplus widened to R45.9 billion in March 2022, supported by elevated commodity prices for key exports that led to the highest trade surplus since June 2021.

SA’s move towards fiscal consolidation received positive news during the month, as data for the full 2021/22 fiscal year indicated that revenue was R33 billion above the original budget estimate and expenditure was R9 billion lower. This translates to an improved deficit to GDP ratio of 4.9%, compared to the original estimate of 5.5%.

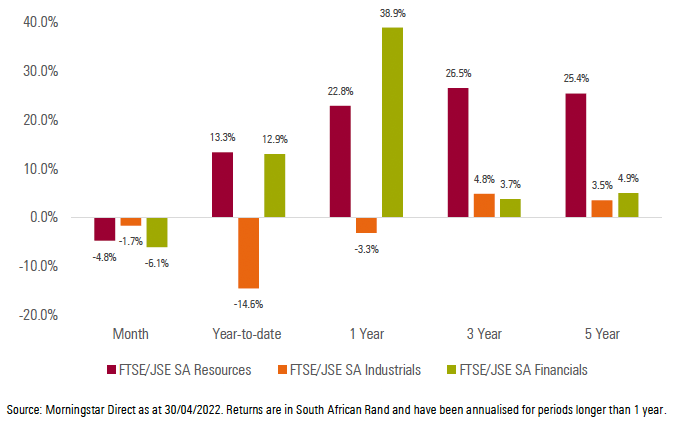

All local equity sectors ended the month lower, with Financials (-6.1%), Resources (-4.8%) and Industrials (-1.7%) all delivering negative performance.

Exhibit 2: SA Sector Performance (total returns)

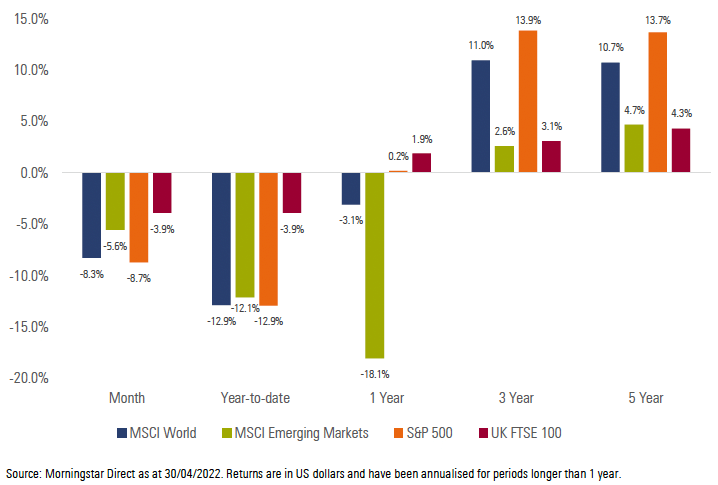

Most of the major developed equity markets ended the month in negative territory, as global geopolitical concerns and elevated inflation prints (and possible higher interest rates) led to weak performance from global risk assets. The MSCI World Index delivered a return of -8.3% for the month.

Emerging market equities also struggled during the month, despite outperforming developed equity markets slightly. The MSCI Emerging Markets Index delivered a return of -5.6% for the month.

Most of the major equity markets ended the month in negative territory. The UK’s FTSE 100 (-3.9%), Germany’s FSE DAX (-7.3%), Japan’s Nikkei 225 (-9.6%) and China’s Shanghai SE Composite (-9.8%) all delivered negative performance for the month.

US equities also struggled, with both the S&P 500 (-8.7%) and the technology heavy NASDAQ 100 (-13.3%) both ending the month sharply lower.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios struggled to generate positive performance over the month. This was largely due to weak performance from risk assets including equities and listed property. Rand weakness over the month did provide a tailwind to the performance of global asset classes, however, this was largely insufficient to compensate for negative hard currency returns from major global equity markets. Those portfolios with an income focus ended the month largely flat or with marginal positive performance, assisted by the returns from local inflation linked bonds as well as shorter dated nominal bonds.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation driven approach by allocating assets to the most attractive areas of the market from a reward for risk perspective. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

Market summary

Click on the link below to download April’s market summary.