In March both market and news headlines were dominated by the war in Ukraine. Developed markets were quick to introduce sanctions against Russia and individuals linked to Putin. During the month, markets tried to digest the impact that sanctions would have on both companies and economies worldwide. Most market participants questioned the impact that higher commodity prices (oil and wheat in particular) would have on inflation as well as global growth expectations. The next point to ponder was how central banks would react to the changing landscape.

Global equity markets remained volatile and ebbed and flowed on the news being reported from Ukraine. The US Federal Reserve (Fed) approved a 0.25% rate hike – the first increase since December 2018. Fed officials also signalled an aggressive interest rate hiking path ahead in a bid to control inflation expectations.

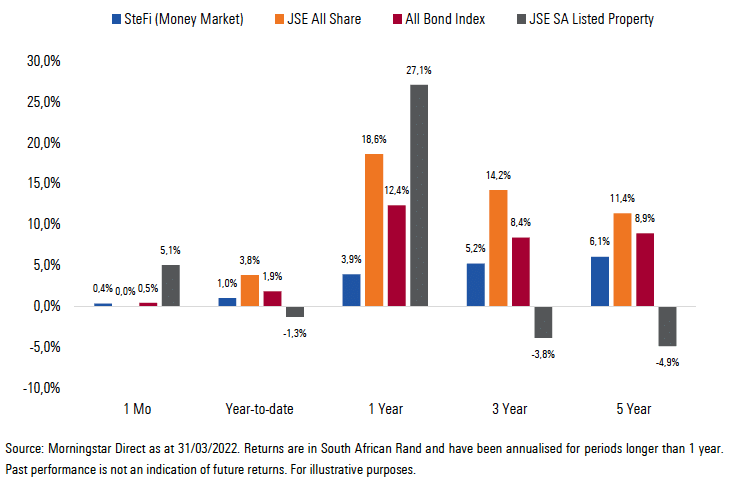

Exhibit 1: SA Market Performance (total returns)

SA equities were flat for March but still managed to outperform Emerging markets. Financials were the main driver of returns in March with the banks being the top performers for the month. Naspers and Prosus continued to struggle in March, with Naspers falling by a further 13.7% in February and bringing the 12-month share price decline to -52.8%. The Capped SWIX Index posted a return of 1.5% for March, bringing the 12-month return to 20.4%.

SA Government Bonds ended the month in positive territory bringing the 12-month return to 12.4%. While it certainly hasn’t been a smooth ride, investors were compensated for holding sovereign debt over cash.

SA Listed property was the best performing asset class in March, ending the month up 5.1% and increasing the year-to-date return to 27.1%. The sector was able to post strong returns despite initial concerns about the war’s impact on other central and eastern European countries.

The rand was resilient in March due to high commodity prices improving our existing current account balance. The local currency moved from trading at R15.45/USD$1 to R14.61/USD$1 over the month.

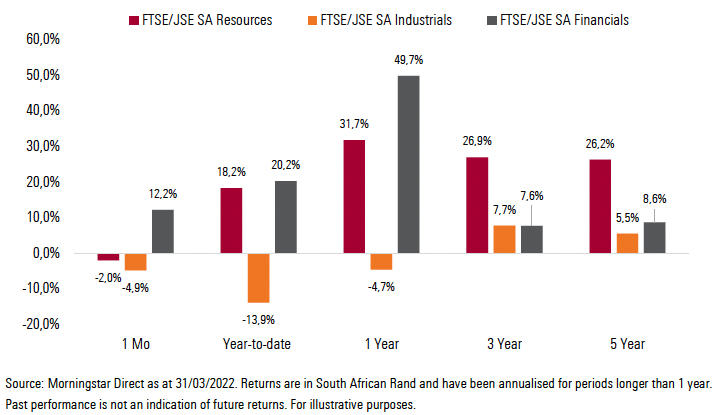

Local equity sectors were boosted by the strong performance of Financials (+12.2%), while Industrials (-4.9%) and Resources (-2.0%) ended the month lower.

Exhibit 2: SA Sector Performance (total returns)

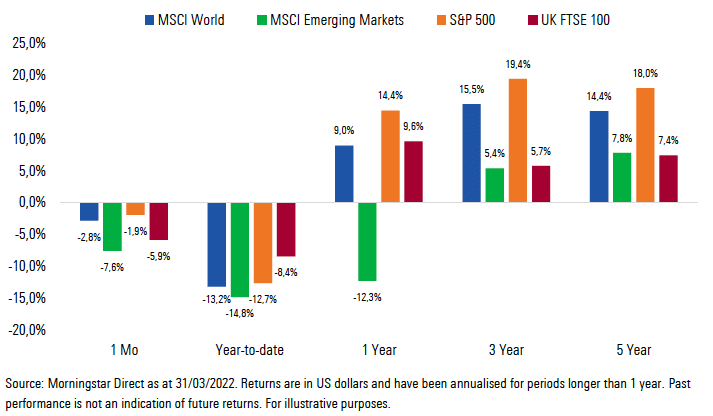

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

While our local portfolios generated negative returns for the month, on a year-to-date basis the portfolios delivered positive returns. This is a result of our healthy exposure to financials and domestic bonds.

Our portfolios with a large offshore exposure have delivered negative returns for the month due to the impact of a stronger currency and muted returns from global markets.

While negative returns are hugely uncomfortable, we would encourage investors not to focus on these two-month return numbers. We have indeed given back some of the returns generated over the past 18 months and we find ourselves in a situation where the range of possible outcomes is wide and impossible to predict.

In times of uncertainty, markets often act in unison, mass selling all assets regardless of quality or valuation. These anomalies do right themselves with time. Returns don’t happen in straight lines, and it seldom occurs when one expects it to. In addition, the long term is just a collection of short runs and having a long-term strategy does not mean that investors won’t have to witness the short-term setbacks in markets. When it comes to investing, patience is rewarded and time in the market remains superior to timing the market.

Market summary

Click on the link below to download March’s market summary.