When there are events like the war in Ukraine, the rand weakening, the price of oil rising to more than $100 a barrel plus unusually high inflation there is bound to be a good deal of market volatility.

In recent weeks investment markets have been tossed back and forth by speculative headlines regarding the possible Russian invasion of Ukraine. When Russia then invaded Ukraine, the US S&P 500 index fell into a correction for the first time in two years, joining the Nasdaq Composite. (A correction is defined as a drop of more than 10% but not more than 20%.)

An event like Ukraine might not be unique but, nevertheless, the volatility and uncertainty it causes makes it very difficult for investors to come to terms with.

How should investors best attempt to handle geopolitical risks in portfolios?

A recent article by our Global Chief Investment Officer, Dan Kemp, sets out four ways investors might typically react to geopolitical risks – some more sensible than others.

- The first is predicting and gambling: where investors try to predict the outcome of the event and then guess the impact it will have on the market. If they turn out to be correct, it could make them seem market experts, but more often than not such investors, and most market participants, get it very wrong.

- The second is the flight instinct: when faced with market volatility and panic some investors prefer to sit and wait, move to cash or what are deemed safe-haven assets (like gold). The problem with this approach is that the market tends to throw some curveballs and the opportunity cost of not being invested could be big.

- The third is remembering valuation and the impact that geopolitical risks would have on the intrinsic value of investment markets which requires a rational framework and immense discipline.

- The fourth and most important is holding tight and focusing on the long term. Most of us know that “long term” is the right strategy when it comes to careers, relationships – or anything that compounds. But saying “I’m in it for the long run” is a bit like standing at the base of Mount Everest, pointing to the top, and saying, “That’s where I’m heading.” Well, that’s nice. Now comes the test.

Given the recent and expected continuation of investment market volatility so far in 2022, what lesson can we remember when we are trying to think and act long term?

The long run is just a collection of short runs you have to put up with.

Long-term thinking can, to some extent, be a deceptive safety blanket that investors assume allows them to bypass the painful and unpredictable short run. Unfortunately, this is very rarely the case. As can be seen in the graph below, it might actually be quite the opposite – the longer your time horizon the more calamities, geopolitical events, inflation scares, tech bubbles, great depressions, financial crises and disasters you’ll experience.

The reality is that part of long-term investing is dealing with short term pain, and you will need to embrace downturns throughout your investing journey. Annual return and drawdown data of the S&P 500 show that – although over the last 42 years we only ended up with an annual negative performance in nine out of the 42 years – every single year over that period had a drawdown or temporary setback, and each of those for very different reasons.

The importance of building robust portfolios

The most powerful protection against market volatility and uncertainty is diversification within portfolios. Both the Maximus/Morningstar SA portfolios and our Global Managed Portfolios have been constructed to ensure exposure to areas of high conviction while maintaining diversification across different regions, sectors, and asset classes.

Our investment views regarding the Russia/Ukraine crisis in a nutshell

- From current levels, a wide range of potential scenarios and outcomes are possible going forward. As multi-asset investors, we should try to avoid predicting these pathways and instead look at the potential implications across assets.

- Energy prices are an area we believe will be heavily impacted.

- During wars and conflicts, the historical track record of the equity market is mixed, with some conflicts such as the Crimea invasion in 2014 leaving equity markets barely changed. Those with a long time horizon will likely be well placed staying invested, statistically speaking.

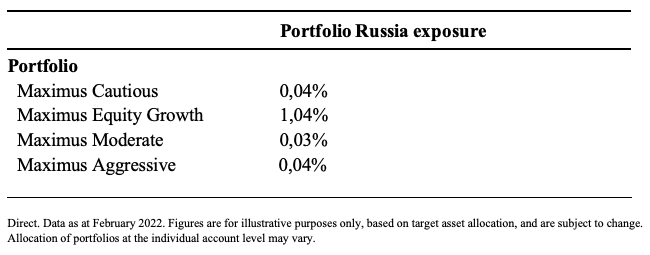

How much exposure do Maximus/ Morningstar portfolios have to Russia?

Russia has very small equity exposure in the global indexes, making up only 3.2% of the MSCI Emerging Markets Index and only 0.4% of the global stock market (measured by the MSCI AC World Index). Ukraine has no exposure in either index.

When we consider the Morningstar Global Managed Portfolios (Global Cautious, Global Balanced and Global Growth) these portfolios have limited exposure to Russian Equities as can be seen below:

- Morningstar Global Cautious: 0.38%

- Morningstar Global Balanced: 0.59%

- Morningstar Global Growth: 1.01%

Maximus local portfolios have very little exposure to Russia as can be seen in the below table:

While the human cost of military action is immeasurable, the stock market reaction to an invasion of Ukraine may be similar to those of the past with little measurable impact for well diversified investors.

How are we reacting to the threat of a downturn?

Should investors be worried about potentially higher inflation, the global portfolios hold sectors that will benefit from higher inflation like commodities, energy and high-quality defensive companies with pricing power. If the worry is a sell-off in US markets, the portfolios are underweight the US and we have allocated to attractively valued parts of the market that include the UK, Europe and Japan. If the main concern is the invasion of Ukraine, the portfolios are diversified across regions with a small position to direct Russian equities.

As we move through this latest period of market volatility, Morningstar Investment Management’s 90-strong investment team continues to prioritise research overreaction, digging deeply into the risks and opportunities presented by the 500+ asset classes we cover to identify those that are unusually attractive or unattractive. Alongside this, the portfolio managers are continually testing the portfolios by simulating different scenarios to ensure that they remain robust to a broad range of potential economic outcomes rather than simply those that dominate the headlines today.

We encourage investors to take the approach of navigating this unknown territory with caution, to diversify smartly, focus on the long term and to pay careful attention to valuations.