Global equity markets started the month of November on a positive footing, however, news of the Omicron variant of Covid-19 and the US inflation print coming in ahead of expectations led to a flight to safety to perceived safe havens including developed market government bonds.

Comments by US Federal Reserve Chair Jerome Powell to the Senate Banking Committee that the threat of higher inflation has increased and that it may be appropriate to bring forward the tapering of bond purchases also weighed on market sentiment.

US President Joe Biden’s $1 trillion infrastructure bill was signed into law during the month; however, President Biden’s $1.75 trillion social spending bill is yet to pass the Senate.

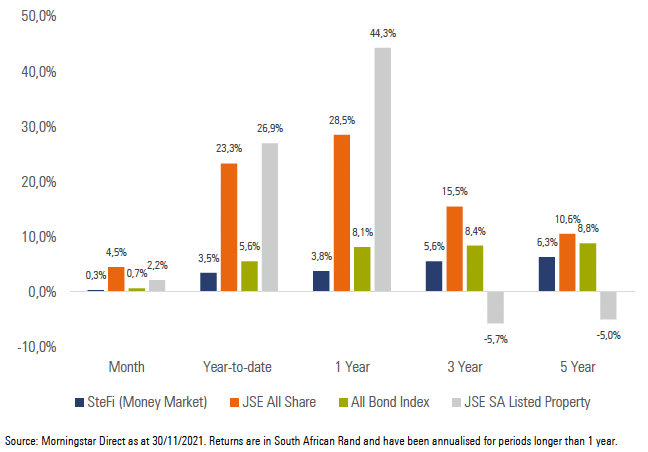

Exhibit 1: SA Market Performance (total returns)

South African equities bucked the global trend, managing to deliver strong performance in the month of November, driven largely by Resources and rand hedge Industrial counters, which were supported by a weaker rand over the month.

Local bonds managed to eke out a positive return, despite significant volatility during the month on the back of domestic economic and fiscal news as well as the global risk off environment which resulted in a flight to safe haven assets.

Local listed property also managed to deliver positive performance for the month, as the sector continues to show stabilization in vacancies, an improvement in collection rates and a reduction in pandemic related concessions (particularly in the retail and industrial sectors).

The rand was weaker against most of the major developed market currencies over the month, largely driven by the global risk off environment which resulted from the discovery of the Omicron variant of Covid-19.

The South African Reserve Bank’s (SARB) Monetary Policy Committee (MPC) met during November and decided to increase the repo rate by 0.25% to 3.75%. Despite the increase in interest rates, there was a lack of consensus among the MPC members, with 2 of the 5 members preferring to keep interest rates on hold.

The new Minister of Finance, Enoch Godongwana, delivered his first Medium Term Budget Policy Statement (MTBPS) in early November. Despite an improved outlook compared to the February budget (largely due to higher commodity prices) and a continued commitment to fiscal consolidation, many difficult decisions have been pushed out to the February 2022 national budget.

SA headline CPI remained unchanged at 5.0% year-on-year for October (from 5.0% in September). Food and non-alcoholic beverage prices moderated during the month; however, this was offset by higher transport prices due to the increase in the fuel price.

The results of South Africa’s local government elections were announced in early November, with the ANC securing less than 50% of the vote (46%) for the first time since the advent of democracy.

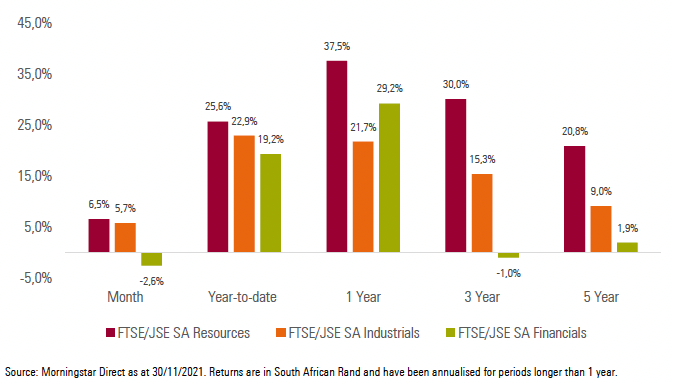

Local equity sectors had mixed performance for the month, with Resources (+6.5%) and Industrials (+5.7%) delivering strong performance, while Financials (-2.6%) ended the month lower.

Exhibit 2: SA Sector Performance (total returns)

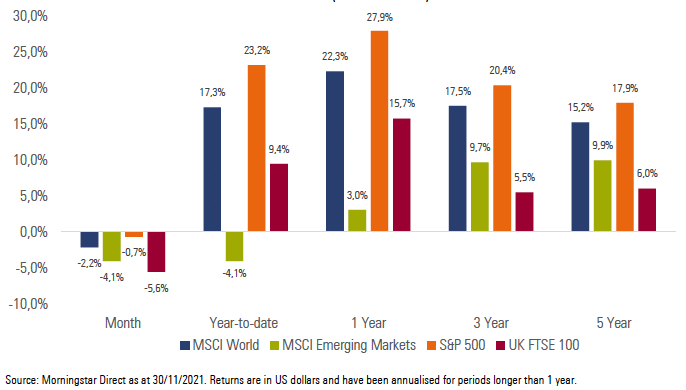

Most of the major developed equity markets ended the month lower, as inflation fears, and the discovery of a new Covid-19 variant impacted investor sentiment. The MSCI World Index delivered a return of -2.2% for the month.

Emerging market equities also struggled, underperforming developed market equities over the month. The MSCI Emerging Markets Index delivered a return of -4.1% for the month.

Most of the major equity markets ended the month in the red. Japan’s Nikkei 225 (-3.3%), the UK’s FTSE 100 (-5.6%) and Germany’s FSE DAX (-6.4%) all delivered poor performance for the month. China’s Shanghai SE Composite (+0.9%) bucked the global trend slightly, managing to eke out positive performance for the month.

US equities delivered mixed performance, with the S&P 500 (-0.7%) ending the month in the red, while the technology heavy NASDAQ 100 (+1.9%) ended the month higher.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios managed to generate positive returns over the month. This was largely driven by strong performance from local equities, while offshore allocations had a strong tailwind from rand weakness. Those portfolios with an income focus managed to generate decent returns over the month, despite significant volatility in the local bond market on the back of political, economic, and pandemic news.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation driven approach by allocating assets to the most attractive areas of the market from a reward for risk perspective. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

Market summary

Click on the link below to download November’s market summary.