In the words of Albert Einstein; “The future is unknown, but a somewhat predictable unknown. To look to the future, we must first look back upon the past.” When it comes to investments, the future is especially unknown. What is especially worrisome is the number of individuals that make a living out of predicting the markets and the future. No, we’re not referring to tarot card readers or fortune tellers – well, not per se. Even though the median forecast is of no value and, in most cases, completely incorrect, it is worrisome just how many people actually make a living in this manner.

Next time leave the forecasting to the fortune tellers – it will serve you much better, to spend your time learning about how to navigate your emotions during uncertain times and turbulent markets.

Markets keep moving up and down, and so too do investor’s emotions. This is understandable – it is, after all, our hard-earned money we’re talking about. It’s only natural that many investors have now grown tired of stomaching this unpredictable and uncertain rollercoaster ride and would much rather prefer to place their feet on solid ground. In the world of investments, the rollercoaster ride is equities and cash is seen as the solid ground.

During volatile times, people find comfort in cash – a natural reaction – even if (more often than not) it is detrimental, as investors panic-sell assets to raise cash after a period of losses. In early 2020, we saw the S&P 500 plunge from an all-time high due to market uncertainty regarding the looming pandemic. The opposite, however, was true for money market funds, which saw its assets under management jump by close to 20% (or as much as $685 billion in March of 2020) posting the highest monthly inflow in, at least, three decades.

In the wise words of Warren Buffett, we want to “be greedy when others are fearful and fearful when others are greedy”.

Good luck in predicting what happens from one year to the next

The problem is – we have no idea when stocks will bottom or what the return of the market will be in the next week, month or even year. Maybe stocks will bottom today? Maybe they will reach a peak in a week…or a year. Who knows?

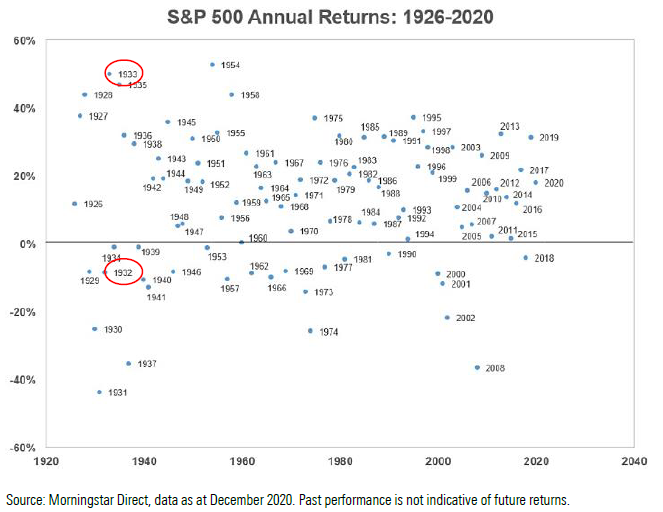

The graph below illustrates this point perfectly – showing the annual returns of the S&P 500 since 1926. Trying to forecast what will happen from one year to the next is very difficult and somewhat of a pointless exercise. For example, if we consider that in 1932 the market posted a negative return, fast forward to 1933 we see a close to 60% return, and then in 1934, the market jumped back into muted territory.

A forecast you can bet on – the longer you are invested, the better your odds of positive returns

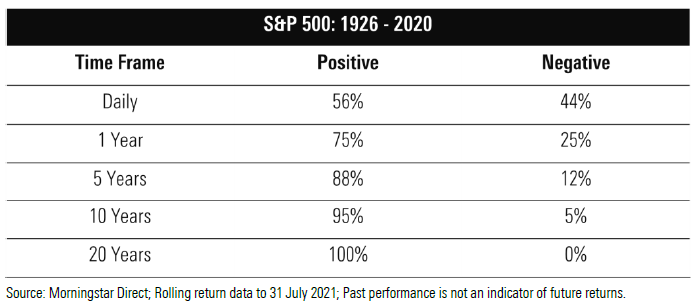

While it is very difficult to predict what will happen in markets, the longer you remain invested the better your odds of positive returns. The below table illustrates this point where if we take the same range of data (S&P 500 since 1926) and look over different time periods, on a daily basis you have a 50/50 chance of ending up either with a negative or a positive return. As your investment horizon increases the number of positive observations increase and over a 10-year time period you have close to a 100% chance that your return will be in positive territory.

Many people compare the stock market (or equities) to a casino but in a casino, the odds are stacked against you. The longer you play in a casino, the greater the odds you’ll walk away a loser because the house wins based on pure probability. It’s just the opposite in the stock market.

The longer your time horizon, historically, the better your odds are at seeing positive outcomes.

Drawdowns are inevitable

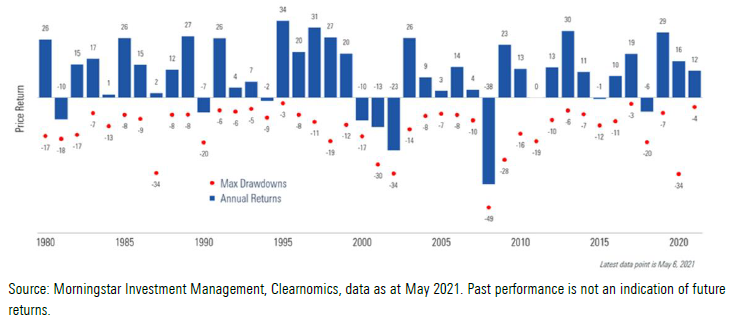

Even if you have a longer time horizon and the odds of positive returns are in your favour, that does not excuse you from all the short term setbacks that do happen in markets. The below graph shows the annual returns of the S&P 500 in the blue bar and the maximum drawdown (i.e. the maximum loss from a peak to a trough of a portfolio, before a new peak is attained) in the red dots.

Although the S&P 500 has provided investors with positive returns in 33 of the 42 years every single year has had a drawdown that investors have had to stomach.

The biggest gains are more than often followed by the biggest drops – and vice versa.

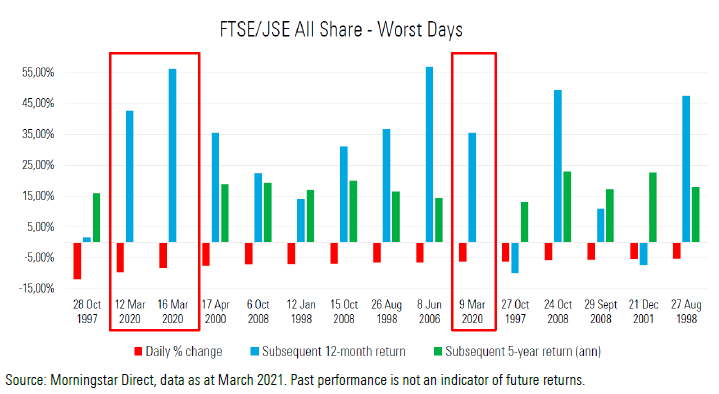

The best days often do come after the worst. When we look at the local market, South African equities experienced three of the largest one-day losses during the March 2020 sell-off.

The below graph shows:

- the 15 worst days on the JSE (the red bars) since the end of June 1995 and how the local market reacted after the

- The blue bars show the 12-month returns investors experienced after the worst day and,

- the green bars show the five-year annualised returns after the drawdown.

As an example, during the 2008 global financial crisis on 06/10/2008, there was a loss of -7.12% for the day but the subsequent one-year return amounted to 22.41% and the annualised five- year return was 19.24%.

Another great example is the recent Covid sell-off in March 2020. During this time, we saw two of the three worst daily drawdowns since 1995 (in March 2020). The COVID-19 outbreak and market volatility dominated the news and investors started to question and second-guess their investment strategies. As hard as it is to do nothing, it served investors well not to flap about in disarray and remain calm as we saw the market having a great rebound following the drawdown.

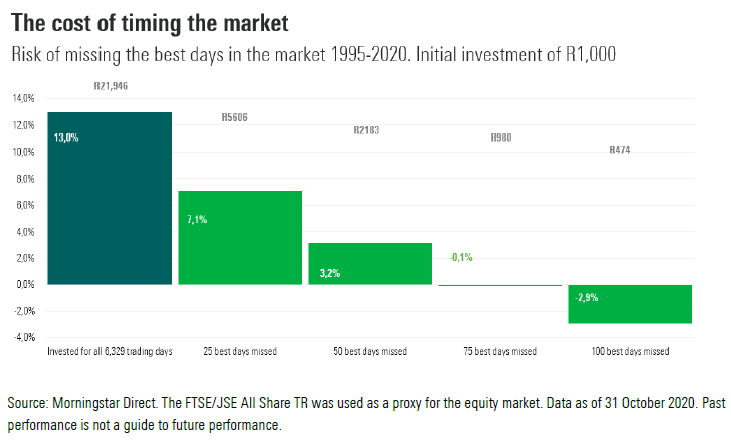

Time in the market is superior to timing the market

It’s tempting to try to time the market, but that requires two important timing decisions — when to sell and when to buy. A few small miscalculations of either move can have a significant impact on the results – that is, how much you gain, or how much you lose. Investment professionals may sound like broken records when they advise investors to sit tight when it comes to dealing with the uncertainty of markets, but the numbers simply don’t lie.

As seen below, missing out on only the top 25 performing days in the market over the past 25 years would cut the gains on an R1 000 investment from an ending value of close to R22 000 to R5 606.

Investing in the equity market is a long-term pursuit and is best used to reach long-term goals such as retirement. As the saying goes – a river cuts through a rock, not because of its power, but its persistence. A big part of wealth creation is avoiding the biggest mistakes and disinvesting into safe havens in times of uncertainty is one of the most well-known actions to avoid.