Global equity markets performed poorly in September, as slowing global growth, concerns around the spread of the Covid-19 Delta variant and liquidity concerns at China’s second largest property developer, Evergrande, dampened risk appetite.

Evergrande indicated during the month that the company has cash flow problems, with reports surfacing that it is at risk of defaulting on money borrowed from China’s shadow banking system. This comes on the back of increased regulatory scrutiny in China from the ruling Chinese Communist Party, with the recent issues at Evergrande raising questions about the overall health of the Chinese economy.

The US Federal Reserve (Fed) met during the month, with the Fed expected to announce the tapering of asset purchases at its next meeting in early November, with the goal of completing its balance sheet expansion midway through 2022. This would suggest that the Fed will shrink its current $120 billion per month quantitative easing programme by approximately $10-$15 billion per month.

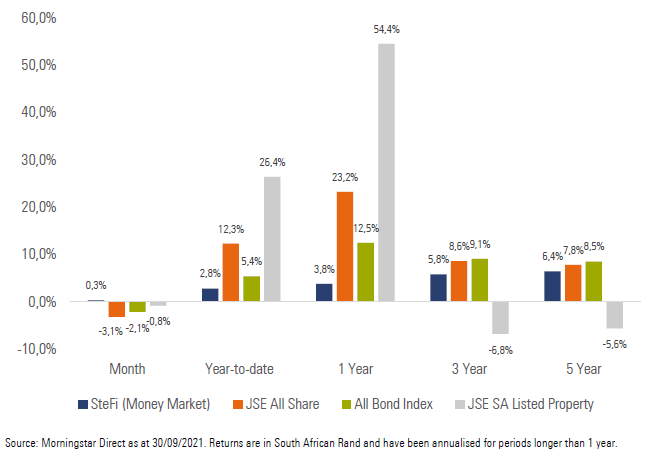

Exhibit 1: SA Market Performance (total returns)

South African equities tracked global markets lower during the month, as poor performance from Resource counters and large Industrial index constituents weighed on the performance of the local equity index.

Local bonds had a tough month, ending lower, as global risk aversion and expectations of the tapering of asset purchases in the US lead to higher yields (and lower prices) on SA bonds.

Local listed property ended the month slightly in the red, as the sector continues its slow recovery from rental relief provided as a result of Covid-19, with many counters prioritising balance sheet improvement, resulting in lower-than-average distribution payments.

The rand was weaker against most of the major developed market currencies, as global risk aversion and a stronger US dollar acted as headwind to the performance of emerging market currencies.

South Africa moved to an adjusted level 1 lockdown on 1 October, as Covid-19 infections continued to decline across the country, which allowed President Cyril Ramaphosa to lift restrictions slightly.

The South African Reserve Bank’s (SARB) Monetary Policy Committee (MPC) announced that interest rates will remain on hold at its meeting in September, which was largely expected, despite the SARB assessing the risks to the short-term inflation outlook to be to the upside.

In terms of the GDP growth outlook, the SARB announced that they expect growth for 2021 to be significantly higher at 5.3%, largely due to the stronger Q1 and Q2 GDP prints as well as the impact of historical revisions. What is of more concern, however, is the downward revision of expected GDP growth for 2022 (to 1.7% from 2.3%) and 2023 (to 1.8% from 2.4%), which is indicative of the fragile state of the SA economy.

SA headline CPI moved higher to 4.9% year-on-year for August (from 4.6% in July), as rising transport and food prices made up the largest components of the inflation increase during the month, the former affected by the 91c per litre petrol price hike during August.

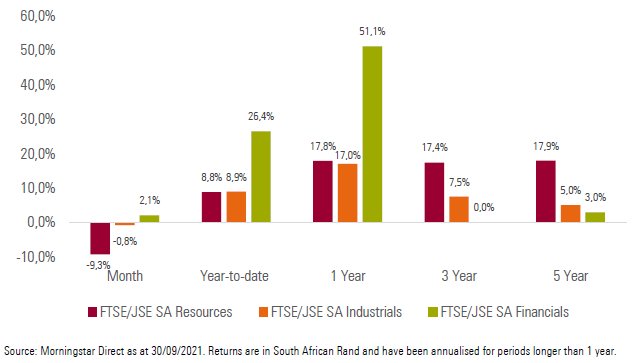

Local equity sectors had mixed performance for the month, with Financials (+2.1%) faring better than both Industrials (-0.8%) and Resources (-9.3%).

Exhibit 2: SA Sector Performance (total returns)

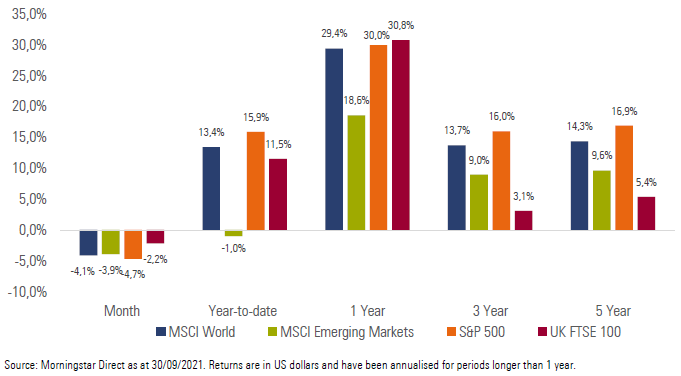

Most of the major developed equity markets ended the month lower, as global growth concerns and the spread of the Covid-19 Delta variant weighed on investor sentiment. The MSCI World Index delivered a return of -4.1% for the month.

Emerging market equities also ended the month in the red, weighed down by poor performance from some of the major commodities. The MSCI Emerging Markets Index delivered a return of

-3.9% for the month.

Most of the major equity markets ended the month with poor performance. The UK’s FTSE 100 (-2.2%) and Germany’s FSE DAX (-5.4%) ended the month lower, while China’s Shanghai SE Composite (+0.7%) and Japan’s Nikkei 225 (+3.9%) bucked the global trend slightly with positive performance.

US equities delivered poor performance, with both the technology heavy NASDAQ 100 (-5.7%) and the S&P 500 (-4.7%) ending the month in negative territory.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios struggled to generate decent returns over the month. This was largely driven by weak performance from SA equities and bonds. The weaker rand over the month acted as a slight tailwind to the performance of offshore allocations, however, this did not offset the weak performance from global equities in hard currency terms. Income focused investors also struggled to generate decent returns over the month, as the local bond market came under pressure from concerns around the tapering of asset purchases in the US.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation driven approach by allocating assets to the most attractive areas of the market from a reward for risk perspective. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

Market summary

Click on the link below to download September’s market summary.