Global equity markets performed strongly in August, with many major global equity indices reaching new highs during the month, despite continued concerns around the spread of the highly contagious Covid-19 Delta variant across the globe.

The US Federal Reserve (Fed) continued to allay fears of interest rate increases, with Fed Chair Jerome Powell reiterating his cautious stance at the Jackson Hole Economic Symposium held towards the end of August. Powell did concede, however, that the tapering of bond purchases is likely to start at the end of 2021.

Powell’s dovish comments, as well as strong earnings updates from corporates, drove US equities to new highs, with the S&P 500 recording a seventh consecutive month of positive returns, its longest winning stretch since 2018.

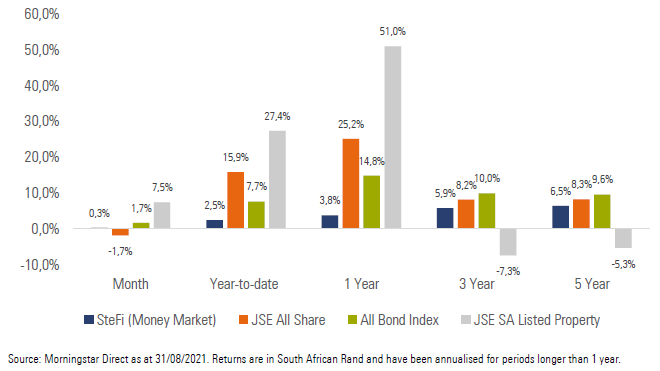

Exhibit 1: SA Market Performance (total returns)

South African equities ended the month lower, as weak performance from Resource counters, as well as large index constituents Naspers and Prosus, weighed on the performance of the local equity index.

Local bonds ended the month higher, as long dated nominal bonds delivered strong performance during the month and the nominal curve continued to flatten during August.

Local listed property rebounded sharply in August, as sentiment towards the sector improved on the back of the move to an adjusted level 3 lockdown on 26 July and many REITs reporting better than expected recoveries from the riot damage caused by the civil unrest in July.

The rand was stronger against most of the major developed market currencies, despite trading in quite a wide range during the month, in line with changes in global sentiment towards emerging market currencies.

In terms of the Covid-19 response, the country remained on an adjusted level 3 lockdown, despite a decrease in the number of daily recorded infections during the month. Registration and vaccination for 18–34-year-olds opened on 20 August, with 12.6 million vaccines having been administered by the end of August.

SA headline CPI moved lower to 4.6% year-on-year for July (from 4.9% in June), as fuel inflation continued to moderate, and SA inflation remained relatively muted due to weak pricing power in the local economy.

SA’s trade balance came in at a surplus for August (R37 billion), following a revised surplus for July of R54 billion, as exports declined 11% month-on-month to R145 billion, higher than the 1% month-on-month decline in imports.

StatSA’s periodic rebasing and reweighting of the national accounts data showed that the nominal size of the economy has increased by 11% from previous estimates, resulting in a lower- than-expected fiscal deficit and debt to GDP (71% at the end of 2020 compared with the previous estimate of 79%).

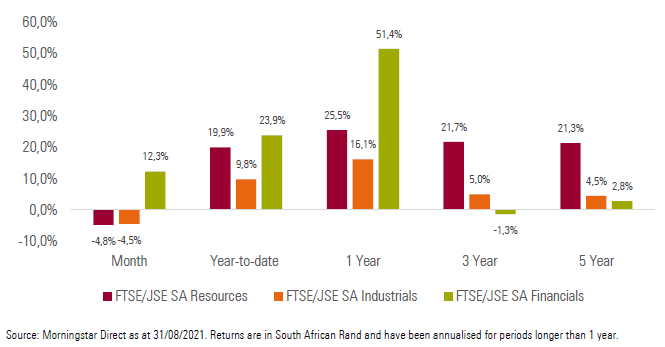

Local equity sectors had mixed performance for the month, with Financials (+12.3%) faring better than both Industrials (-4.5%) and Resources (-4.8%).

Exhibit 2: SA Sector Performance (total returns)

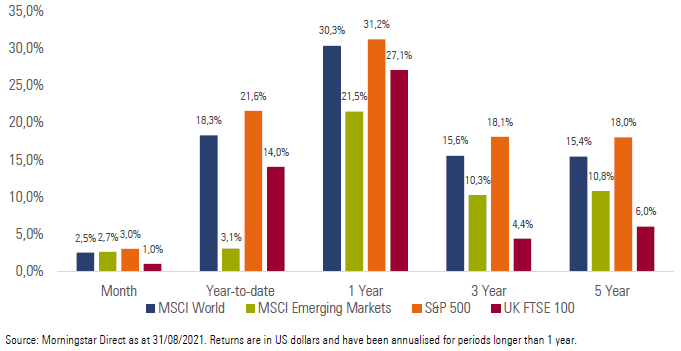

All major developed equity markets delivered decent performance for the month, with many global equity indices reaching new all-time highs during the month. The MSCI World Index delivered a return of +2.5% for the month.

Emerging market equities delivered performance largely in line with developed markets over the month. The MSCI Emerging Markets Index delivered a return of +2.7% for the month.

Performance from the major equity markets was largely positive, with China’s Shanghai SE Composite (+4.2%), Japan’s Nikkei 225 (+2.9%), Germany’s FSE DAX (+1.4%) and the UK’s FTSE 100 (+1.0%) all ending the month in the black.

US equities continued to deliver strong performance, with the technology heavy NASDAQ 100 (+4.3%) and the S&P 500 (+3.0%) both ending the month higher.

Exhibit 3: International Market Performance (total returns)

Impact on client portfolios

Most portfolios managed to deliver decent performance for the month. This was largely driven by strong returns from global equities, as well as local bonds and property. The stronger rand over the month acted as a slight headwind to the performance of offshore allocations. Income focused investors also managed to generate decent returns over the month, as the local bond market ended August with strong performance.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation driven approach by allocating assets to the most attractive areas of the market from a reward for risk perspective. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

Market summary

Click on the link below to download August’s market summary.