Negative market sentiment continued in September, resulting in the first negative quarter of 2023 for most asset classes. The majority of asset classes closed the month in negative territory, largely due to cautious comments from global central banks, lofty equity valuations and ongoing signs of slowing economic growth. Inflation has trended lower during the past few months, leading most central banks to keep interest rates unchanged in their September meetings. However, they remained cautious about ongoing inflation risks, increasing the likelihood of a prolonged period of higher interest rates to manage inflation. This uncertainty led to a widespread sell-off across various assets, including the US 10-year government bond, which saw its yield at its highest in 17 years.

Most policymakers moved to keep interest rates unchanged this month, however, they continued to caution of upside risks to inflation. The ECB was one of the few developed markets to hike rates during its September meeting. The ECB hiked interest rates for the 10th consecutive time to 4.5%, ahead of expectations. The ECB signalled that it is likely done tightening policy, as inflation has trended downwards, but is still expected to remain high. The US Federal Reserve (Fed) kept the target interest rate at a 22-year high of 5.5% in its September 2023 meeting, following a 0.25% hike in July, and in line with market expectations. The Fed signalled that there could be a further hike later this year. The Bank of England held its policy interest rate at 5.25% on September 21st, keeping borrowing costs at their highest level since 2008, as policymakers opted for a wait-and-see approach following the latest inflation and labour data, which suggested that the accumulated impacts of previous policy tightening might be taking effect.

Developed market inflation numbers produced varied results last month, however, most remained above central banks’ inflation targets. The annual inflation rate in the US moved higher to 3.7% (year-on-year to the end of August) from 3.2% in July and above market forecasts of 3.6%. Oil prices have been on the rise in the past two months, which coupled with high base effects pushed inflation higher. The core inflation rate, however, slowed for the fifth month to 4.3% (year-on-year to the end of August), in line with market expectations. China’s consumer prices rose by 0.1% (year-on-year to the end of August 2023), compared with market forecasts of 0.2%. The inflation rate in the euro area declined to 4.3% (year-on-year to the end of August), reaching its lowest level since October 2021 and falling below the market consensus of 4.5%. Consumer price inflation in the United Kingdom eased to 6.7% (year-on-year to the end of August), from 6.8% in the previous month, below the market consensus of 7.0%.

Turning to unemployment, most global developed markets posted an uptick in unemployment, indicating that the labour market may be cooling off after months of monetary policy tightening. The unemployment rate in the US rose to 3.8% (to the end of August 2023), from a level of 3.5% recorded in July, the highest since February 2022 and above market expectations of 3.5%. The unemployment rate in the United Kingdom rose to 4.3% (to the end of July), ahead of expectations.

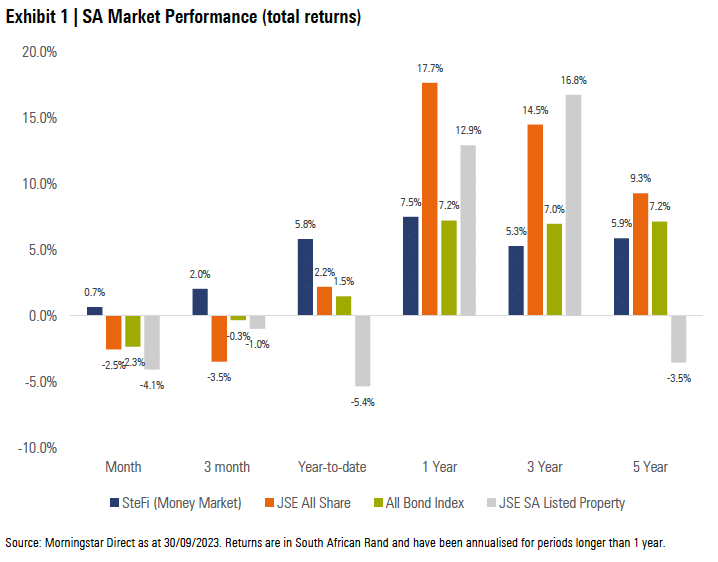

South African asset classes followed global peers lower this month, as both local equities and bonds came under pressure. South African equities reported a negative return for the month, broadly in line with the emerging market complex. However, SA equities outperformed most developed market indices, as commodity linked counters rebounded this month from the poor performance recorded in August. The rand weakened marginally this month on the back of further risk-off sentiment.

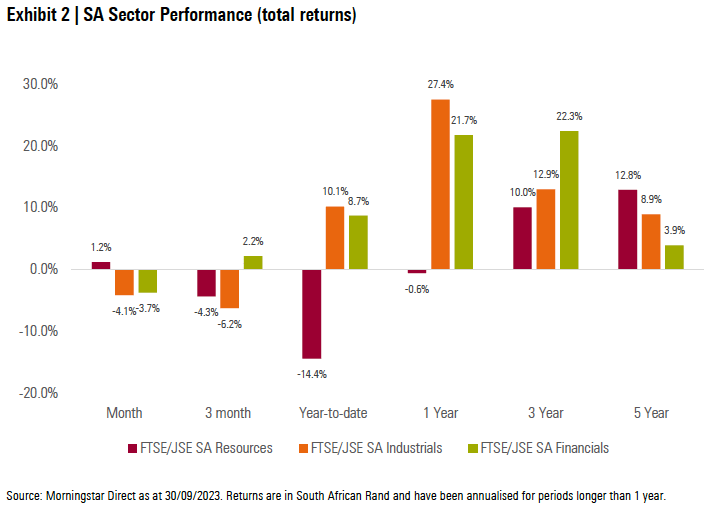

South African equities ended the month lower, as most sectors produced negative returns. Financials produced a negative return this month, driven lower by index heavy weight Firstrand (-13.0%), on the back of results that missed expectations. Resources were the outperformer this month, producing a positive return on the back of index heavy weights BHP Group (+1.7%) and Anglo American PLC (+3.6%) producing strong returns. Industrials ended lower and were the biggest laggard this month, as broad weakness in the sector led to a strong decline.

Local bonds ended the month lower, as the yield curve shifted higher (and prices moved lower) on expectations for higher for longer interest rates. While rates were kept unchanged at the most recent meeting, the hawkish tone from the central bank governor coupled with a concern around the South African fiscal outlook led to a selloff in South African bonds. All eyes will be on the upcoming Medium-Term Budget Policy Statement (MTBPS) scheduled for the 1st of November, which will provide an update on the state of government finances.

Local listed property produced a negative performance this month, lagging the SA equity market. The prevailing risk-off sentiment, coupled with a large decline in the index heavyweight Growthpoint (-10.7%), who produced results that missed expectations, was a major drag on the index’s performance.

South Africa’s annual inflation rate moved slightly higher to 4.8% (year-on-year to the end of August), in-line with market estimates, after four consecutive month-on-month declines. Inflation remains within the South African Reserve Bank’s target range of 3% to 6%. Prices accelerated mostly for housing and utilities (5.5%), driven largely by increases in electricity and other fuels, which increased 15.1%. The annual core inflation rate edged higher to 4.8% (year-on-year to the end of August), above market forecasts of 4.7%. Risks to inflation remain high, as petrol price increases coupled with the rand’s depreciation continue to place upward pressure on inflation.

The South African Reserve Bank kept the repo rate at 8.25% during its September meeting, as anticipated, but emphasized that the fight against inflation was not done. Policymakers cited concerns about the continued depreciation of the rand and the ongoing pressures on inflation. Simultaneously, policymakers slightly raised growth forecasts for this year to 0.7%, from 0.4% in July, while maintaining a 1% forecast for 2024, but noted that electricity and logistical issues continue to threaten the economic outlook.

The current account deficit in South Africa widened to R160.7 billion in the second quarter of 2023, from a downwardly revised R63.7 billion in the prior quarter, but below market expectations of a R178.4 billion shortfall. This was the largest current account gap since Q3 2019. As a ratio of GDP, the current account deficit widened to 2.3% in the second quarter of 2023, from 0.9% in the first quarter.

In terms of other important economic releases: The South African economy grew by 1.6% (year-on-year in the second quarter), above market estimates of a 1.1% increase. The FNB/BER Consumer Confidence Index for South Africa improved to -16 points in the third quarter of 2023, from -25 points in the previous period, the lowest reading in a year.

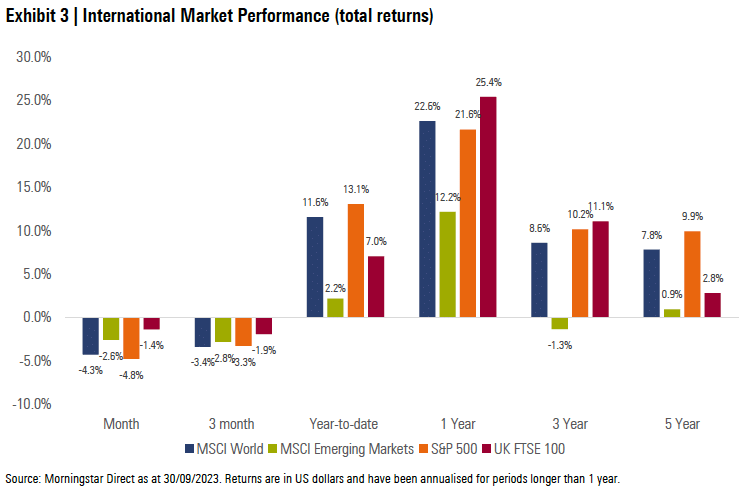

Most of the major developed equity markets ended the month lower this month. The MSCI World Index delivered a return of -4.3%, which was behind that of emerging market peers.

Most emerging equity markets moved lower during the month, on the back of weak equity markets coupled with a strong US dollar. The MSCI Emerging Markets Index ended the month -2.6% lower in September.

Most major global equity markets produced negative returns in September. The UK’s FTSE 100 (-1.4%), Germany’s FSE DAX (-5.9%), Japan’s Nikkei 225 (-4.0%) and China’s Shanghai SE Composite (-0.5%) ended the month in negative territory.

US equities moved lower in September, following global peers. The tech-heavy NASDAQ 100 (-5.0%) posted its largest monthly decline of 2023, as mega-cap technology stocks came under pressure on the back of lofty valuations and the strong performance on a year-to-date basis. The S&P 500 (-4.8%) also ended the month lower, posting its worst monthly performance of 2023.

Impact on client portfolios

From a portfolio perspective, investors struggled to generate meaningful performance in a particularly weak environment during the month of September and for the third quarter. Negative global sentiment towards risk assets pushed South African asset classes lower this month. Global equity markets generated weak hard currency returns this month, on the back of negative sentiment towards risk assets. Rand weakness did act as a minor tailwind to the performance of global allocations, as the local unit was weaker against most of the major crosses during the month. This tailwind was not significant enough to push returns into positive territory.

After the volatile moves of September, we are reminded that economic events such as possible recessions and the uncertainties that come with it bring out behavioural biases and focuses investors on the short term. Moreover, it reinforces the need for robustness and judicious diversification in portfolios. Specifically, we continue to seek exposure to assets that offer strong forward-looking prospects, while balancing risks with defensive exposures.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation-driven approach by allocating assets to the most attractive areas of the market from a reward-for-risk perspective and ensure we build robust portfolios. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

Market summary

Click on the link below to download September’s market summary.